Lending protocols are among the most critical building blocks of the decentralized finance ecosystem. From early over-collateralized lending models to innovations like flash loans, isolated pools, and cross-chain lending, DeFi lending protocols have become essential infrastructure for on-chain financial activity.

Aave is widely recognized as the industry gold standard in the DeFi lending market, with its model shaping countless protocols that followed. Folks Finance emerged amid the rapid rise of multi-chain finance, tackling liquidity fragmentation across blockchains with a unified liquidity architecture.

What Is Folks Finance?

As a decentralized lending protocol built for the multi-chain ecosystem, Folks Finance enables cross-chain lending, asset management, and liquid staking through a unified liquidity architecture.

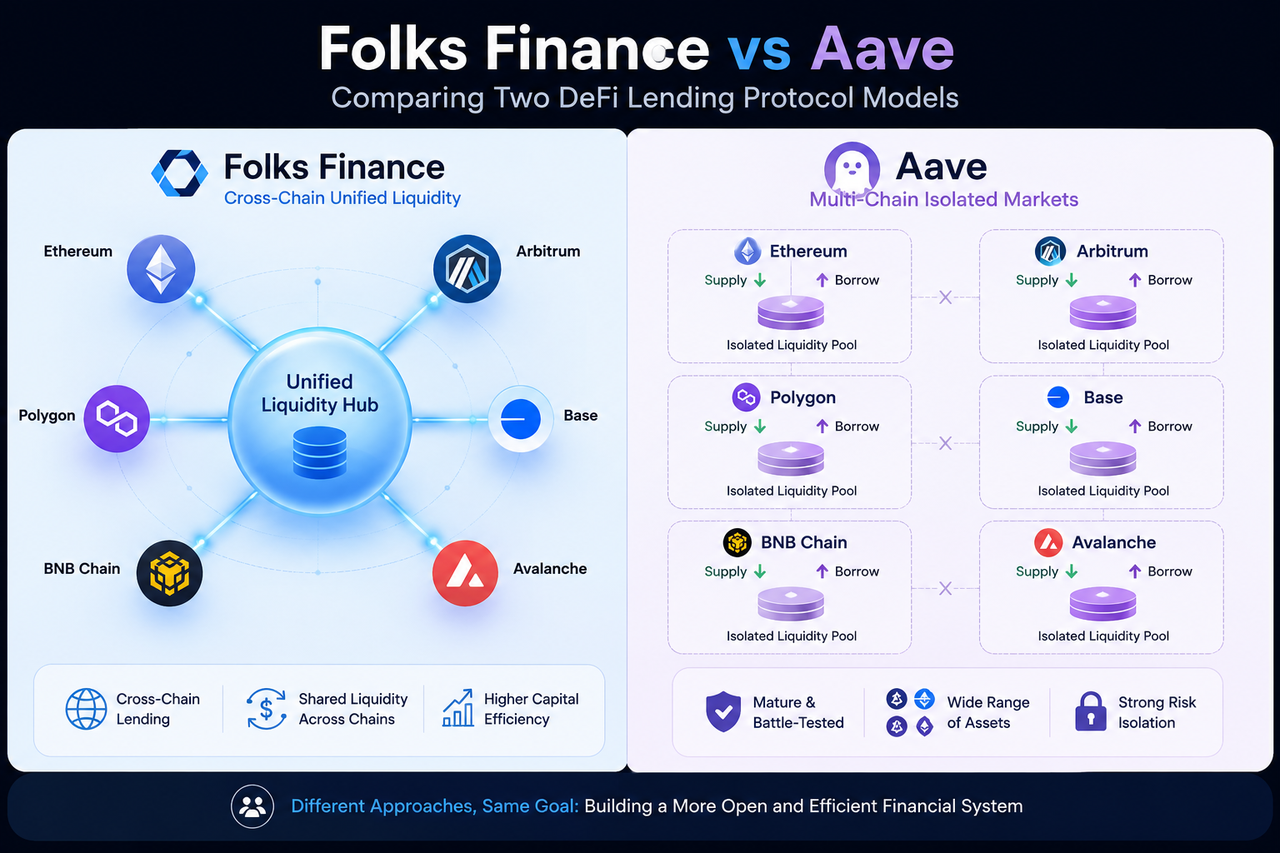

Unlike traditional multi-chain lending protocols that spin up fully independent lending markets for each chain, Folks Finance uses a Hub-and-Spoke model to connect multiple blockchain networks. The protocol aims to boost capital efficiency and simplify the user experience in multi-chain environments by relying on shared liquidity pools.

As DeFi evolves from a single-chain landscape to a cross-chain one, Folks Finance positions itself as cross-chain liquidity infrastructure rather than just another lending platform.

What Is Aave?

Aave is one of the most iconic lending protocols in DeFi and a key driver of modern on-chain lending models.

Aave lets users deposit digital assets to earn interest while borrowing other assets via an over-collateralization mechanism. Originally deployed on Ethereum, it has since expanded to multiple public chains and Layer 2 networks.

Beyond standard lending, Aave pioneered Flash Loans, Isolation Mode, and Efficiency Mode (E-Mode), all of which have left a lasting mark on the entire DeFi lending sector.

Today, Aave stands as a cornerstone of multi-chain DeFi lending infrastructure.

How Do Their Liquidity Architectures Differ?

The fundamental difference between Folks Finance and Aave lies in how they organize liquidity.

Aave uses an independent market architecture. Even though the protocol is deployed across multiple blockchain networks, the liquidity pools on each chain remain isolated. The pool on Ethereum can't directly support lending on Avalanche or Arbitrum.

This model offers strong independence and security isolation, but it also fragments liquidity.

Folks Finance tackles this with a unified liquidity architecture.

The protocol uses a Hub-and-Spoke model to link multiple blockchains, allowing different networks to share a single lending market. A user who puts up collateral on one chain can directly support borrowing on another chain, improving overall capital efficiency.

This design is one of the key things that sets Folks Finance apart from traditional lending protocols.

How Do They Handle Cross-Chain Lending?

Aave's core lending logic still runs on single-chain markets. While users can move assets via third-party cross-chain bridges, the actual lending almost always happens within the same blockchain.

For example, after depositing ETH on Ethereum, a user will typically borrow other assets on Ethereum. If they want to use liquidity on Arbitrum, they'll need to bridge assets over first.

Folks Finance, on the other hand, treats cross-chain lending as a core design goal.

Users can deposit collateral on one chain and borrow assets on another chain. The entire process is coordinated by a unified liquidity layer and a cross-chain messaging system—no need for users to shuttle assets back and forth.

So the real difference isn't whether they support multiple chains; it's whether they natively support cross-chain lending.

How Do User Experiences Differ?

In Aave, each chain has its own independent lending market. Users have to manage positions on different networks separately, keeping an eye on collateral ratios and risk parameters for each chain.

For anyone juggling multiple blockchains, that means constantly switching networks and tracking multiple account states.

Folks Finance, in contrast, aims for a unified account view.

Thanks to its unified liquidity architecture, users can manage lending positions across different chains without maintaining separate accounts for each independent market. That lowers the barrier to multi-chain usage and cuts down on repetitive steps.

As cross-chain finance gains traction, this unified experience is becoming a bigger competitive advantage.

How Do Risk Management Mechanisms Differ?

One of the biggest challenges for any lending protocol is risk management.

Aave's risk control framework has been battle-tested over years of operation. The protocol relies on over-collateralization, oracles, liquidation mechanisms, and risk parameter management to keep the market running smoothly.

Because each chain's market is independent, a problem on one chain usually doesn't spill over to the others.

Folks Finance inherits the traditional lending risk management approach but also has to deal with the added complexity of the cross-chain environment.

Unified liquidity boosts capital efficiency, but it also means the system needs to monitor asset status, price volatility, and account health across multiple blockchain networks at the same time.

That's why a cross-chain messaging system and a unified risk engine are critical parts of Folks Finance's risk management framework.

How Do Their Governance Models Differ?

Both protocols use community governance, but they focus on different things.

Aave's governance revolves around protocol parameter adjustments, new market launches, risk management, and ecosystem growth. AAVE holders vote on-chain to make decisions.

Given Aave's large ecosystem, governance tends to focus more on keeping existing markets stable.

Folks Finance's governance, on the other hand, is closely tied to its cross-chain ecosystem.

Beyond adjusting lending parameters, the community weighs in on which blockchains to support, how to manage unified liquidity, and where to steer the cross-chain infrastructure.

As a result, Folks Finance governance discussions often emphasize ecosystem expansion and cross-chain coordination.

Which Scenarios Are Better Suited for Folks Finance? Which for Aave?

Aave is the better fit for users who want a mature, battle-tested lending market.

Its ecosystem is massive, it supports a wide range of assets, liquidity is deep, and it has a long track record. For standardized lending needs, Aave has become essential infrastructure.

Folks Finance, on the other hand, is ideal for users focused on multi-chain asset management and cross-chain capital efficiency.

If you're constantly reallocating assets across multiple blockchains, the unified liquidity and cross-chain lending mechanism can cut down on capital migration costs and improve asset utilization.

These two aren't strictly competitors—they represent different paths forward for the DeFi lending market.

Core Differences Between Folks Finance and Aave

| Dimension |

Folks Finance |

Aave |

| Core Positioning |

Cross-chain lending infrastructure |

Multi-chain lending market |

| Liquidity Architecture |

Unified liquidity |

Independent market liquidity |

| Cross-Chain Lending |

Native support |

Mostly relies on bridges |

| Capital Efficiency |

Shared unified market |

Independent per chain |

| User Perspective |

Multi-chain unified account |

Multi-chain independent markets |

| Risk Management |

Cross-chain unified risk model |

Chain-level risk isolation |

| Ecosystem Direction |

Cross-chain financial infrastructure |

DeFi lending platform |

Conclusion

Folks Finance and Aave are both DeFi lending protocols, but their design philosophies are clearly different. Aave represents the mature lending market model, offering services through independent markets on multiple blockchains. Folks Finance, by contrast, aims to build a cross-chain lending network using unified liquidity and a Hub-and-Spoke architecture.

As DeFi moves from a single-chain world to a multi-chain one, capital efficiency and liquidity aggregation are becoming ever more important. Aave remains one of the most iconic lending protocols in the industry, while Folks Finance offers a new blueprint for cross-chain financial infrastructure.

FAQs

What's the biggest difference between Folks Finance and Aave?

The biggest difference is their liquidity architecture. Aave uses an independent market model where each chain has its own liquidity pool. Folks Finance uses a unified liquidity architecture that lets multiple blockchains share the same lending market.

Does Folks Finance support cross-chain lending?

Yes. Cross-chain lending is one of Folks Finance's core design goals. Users can deposit collateral on one chain and borrow assets on another chain.

Does Aave support cross-chain lending?

Aave supports multiple chains, but its lending markets typically operate independently. Users can bridge assets across chains, but lending itself happens primarily within a single chain.

Which protocol has higher capital efficiency?

In theory, Folks Finance's unified liquidity architecture can improve overall capital utilization by allowing different chains to share liquidity. Aave uses an independent market model that prioritizes market isolation and risk control.

Do both Folks Finance and Aave use over-collateralization?

Yes. Both protocols mainly rely on over-collateralization, requiring users to put up collateral worth more than the amount they borrow to keep the protocol secure.