OPENAI is a mirror note and contingent payment note disclosed by Gate. Actual OpenAI equity refers to company shares, while traditional Pre-IPO investments typically rely on private transactions or fund agreements.

"Value association" does not mean "identical legal rights." Comparisons should focus on the source of rights, price formation, and settlement terms—not just whether the brand name is the same. If the comparison is limited to "accessing the OpenAI narrative," all three paths may appear similar; but if you ask "who can the holder make a claim against, and for what," the differences become clear.

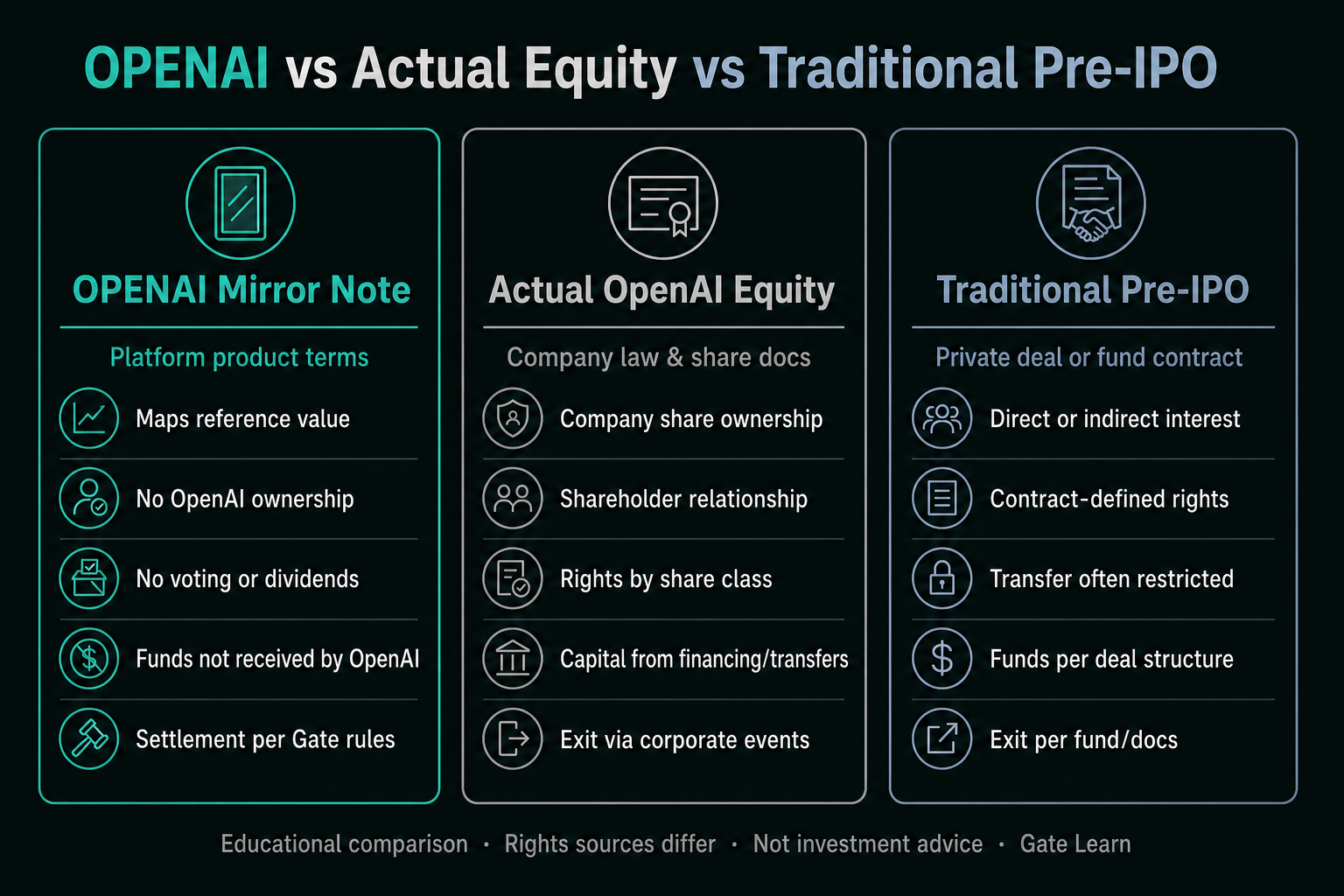

What Is the OPENAI Mirror Note?

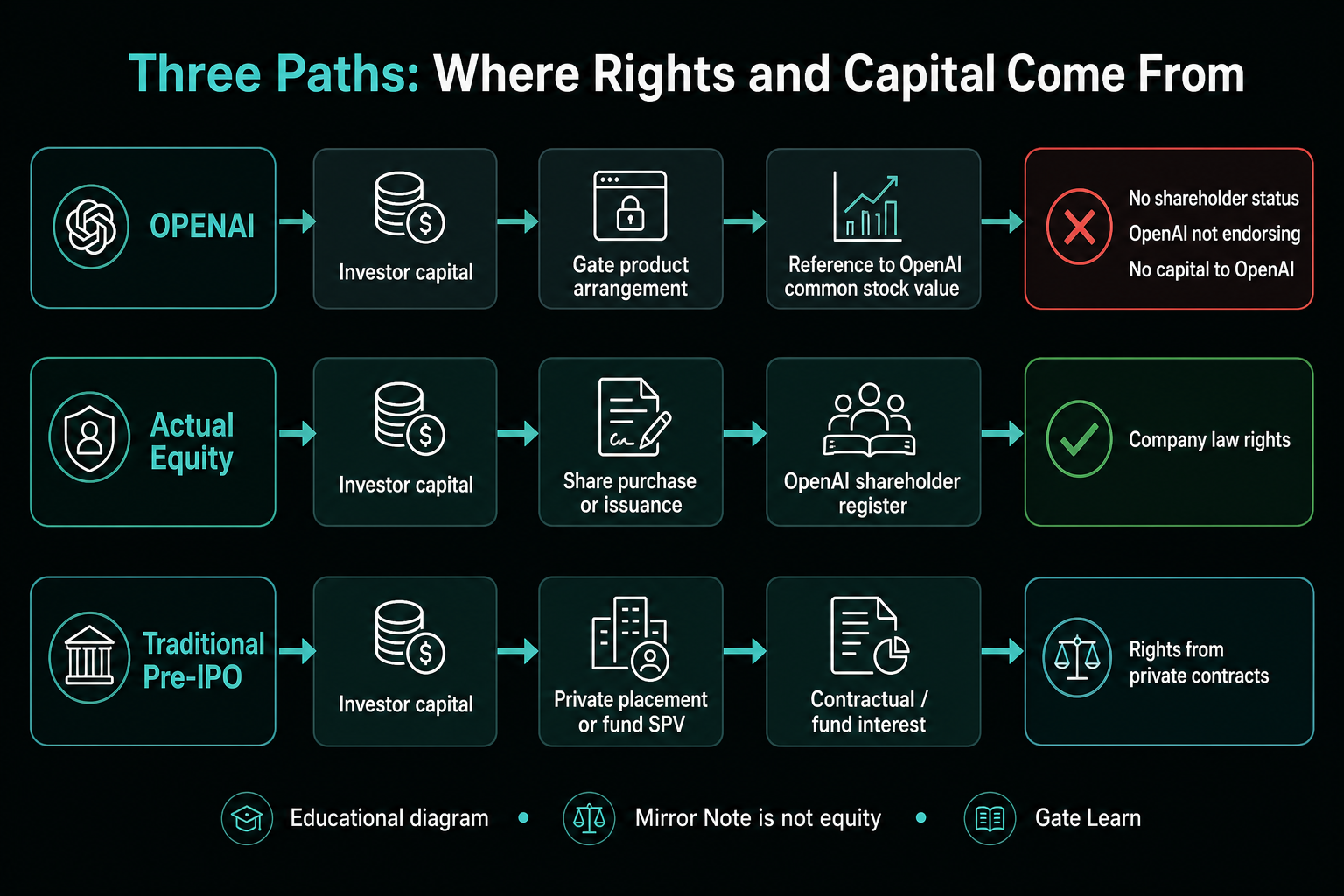

As officially disclosed in both Chinese and English, the OPENAI asset certificate is issued prior to the OpenAI IPO to mirror the company’s pre- and post-listing market value. It is a contingent payment note. Holders receive allocations, transfers, and settlement arrangements according to the product terms—not ownership of company assets or shares. The Gate project page and announcements specify: it does not represent actual stock or shares; it does not establish a legal relationship with OpenAI; OpenAI has not participated, authorized, or endorsed, and does not receive any funds raised.

Therefore, OPENAI should be viewed as a "product that maps reference value according to disclosure rules," not as a "fractionalized company share." This is the foundational premise for all subsequent comparison tables.

What Are Actual OpenAI Equity and Traditional Pre-IPO Investments?

Actual equity refers to company capital established in accordance with company law, articles of association, shareholder registers, and transaction documents. The scope of shareholder rights depends on share class and jurisdiction; the term "shareholding" does not automatically confer full control. Unlisted actual equity often involves transfer restrictions, information rights, and shareholder agreement obligations.

Traditional Pre-IPO investment generally refers to participating in unlisted equity through private placements, secondary share transfers, or fund vehicles before a public listing. Investors may directly hold shares or hold fund units or contractual indirect interests; transfer restrictions and exit conditions are determined by the relevant documents. When distinguishing OPENAI and actual equity, it is essential to separate company-level capital from platform-level note rights. Even when OpenAI is the subject, traditional paths may have entirely different counterparties, disclosure obligations, and exit mechanisms.

How Do Rights and Legal Relationships Compare Across the Three?

| Comparison Dimension |

OPENAI Mirror Note |

Actual OpenAI Equity |

Traditional Pre-IPO |

| Legal Basis |

Gate product terms |

Shares, company documents, and law |

Private placement or fund contracts |

| Company Ownership |

No |

Yes (scope depends on share class) |

Direct or indirect, per contract |

| Voting & Dividends |

Not provided |

Per shares and company arrangements |

Per shareholding or fund rights |

| Legal Relationship with OpenAI |

Not established |

Shareholder relationship |

Depends on structure |

| Fund Destination |

OpenAI does not receive funds |

Depends on financing or transfer |

Per private placement or fund terms |

Image note: All three paths may be linked to OpenAI’s value, but the source of rights and settlement mechanisms differ.

Image note: All three paths may be linked to OpenAI’s value, but the source of rights and settlement mechanisms differ.

How Do Price, Value, and Liquidity Differ?

OPENAI’s value is based on the reference value of common shares and adjustments per the terms; the official implied market value is derived from the committed price and estimated share count—see Implied Valuation and Dilution. Actual equity value depends on share class, transaction, and capital structure; traditional Pre-IPO may also include fund fees, NAV methodology, and lock-up periods. Liquidity should not be compared directly: OPENAI depends on disclosed pre-market and settlement mechanisms, while equity and private rights are typically subject to contractual and regulatory restrictions. Comparing the "prices" of all three paths on the same scale often overlooks the asymmetries in liquidity and rights constraints.

How Do Corporate Actions and Settlement Mechanisms Differ?

OPENAI may adjust calculation bases or holdings in the event of new issuance, stock splits/mergers, or reclassification, as per the terms; it may also circulate pre-market as disclosed, be redeemed after IPO lock-up periods, or be settled in USDT at fair market value upon maturity or certain events. Actual equity corporate actions are governed by company documents; traditional Pre-IPO requires following through private placement or fund distribution and liquidation terms. Settlement counterparties differ: the note path is subject to product rules and platform arrangements, the equity path to company and securities intermediaries, and the fund path to managers and partnership documents.

Image note: Reference units and corporate actions affect mirror calculations through product terms—they do not constitute equity delivery.

Image note: Reference units and corporate actions affect mirror calculations through product terms—they do not constitute equity delivery.

What Are the Risks and Limitations of the Three Paths?

OPENAI’s main limitations are its non-equity nature and reliance on platform rules; pre-IPO uncertainty, pre-market liquidity, and event settlement also pose risks. Because OpenAI is not involved in the product and does not receive funds, holders cannot treat platform disclosures as company financing documents or shareholder communications. Actual equity and traditional Pre-IPO are not "unconstrained channels" either: share class differences, transfer restrictions, information asymmetry, fund-level fees, and exit timing can all affect rights realization.

A common misunderstanding is to compare only "access to the OpenAI name," while ignoring the contractual text. Mirror notes are compared via product pages and announcements; direct equity via shares and company law arrangements; traditional Pre-IPO via private placement memoranda or fund partnership agreements. Any approach that merges the three into a single "OpenAI investment" label loses critical distinctions. The product risk checklist is best used to match qualifications, lock-ups, settlement, and disclaimers to disclosed terms—not to infer rights from product names.

For those researching OpenAI, the core questions are: at the company level, "does one become a shareholder;" at the product level, "which terms govern settlement claims." Only when both are answered is the path classification complete. Identical names are never proof of identical structures.

Summary

Under the "OpenAI" keyword, participation paths should be divided into at least three types: mirror notes, actual equity, and traditional Pre-IPO. OPENAI establishes reference and settlement under Gate’s terms; actual equity is centered on company ownership; traditional Pre-IPO is defined by private placement or fund contracts. The purpose of comparison is to clarify mechanism differences, not to rank the paths; identical names do not imply identical structures.

FAQ

Is OPENAI actual OpenAI stock?

No. OPENAI is an officially defined mirror note and contingent payment note. It only maps reference value and does not transfer OpenAI ownership.

Does holding OPENAI grant voting or dividend rights?

No. Rights are defined by Gate product terms and do not establish a legal relationship with OpenAI.

What is the main difference between OPENAI and traditional Pre-IPO?

OPENAI is a value-mapping note under platform product terms; traditional Pre-IPO typically acquires direct or indirect company capital through private placement or fund contracts.

How do OpenAI corporate actions affect OPENAI?

In the case of new issuance, cancellation, stock splits/mergers, or reclassification, Gate disclosures may adjust calculation bases or holdings; these adjustments do not mean holders directly participate in corporate actions.

How is OPENAI handled if OpenAI does not go public, is acquired, or goes bankrupt?

According to the announcement, if OpenAI is not listed after the maturity date, or in the event of acquisition, merger, or bankruptcy, settlement will be in USDT at OpenAI common stock fair market value. If liquidation results in zero, the product reference value may also be zero.