---

AI workloads feature significantly higher read/write intensity than traditional cloud applications, requiring a tiered storage configuration optimized across throughput, latency, and cost. NAND Flash and SSDs have emerged as the core categories for incremental procurement. SanDisk (SNDK) occupies the segment from NAND manufacturing to enterprise SSD delivery and must be evaluated separately from Western Digital (WDC)'s HDD archive tier and Micron's DRAM memory tier.

Why AI Training and Inference Drive Higher Storage Data Layer Demand

AI training and inference impose demanding requirements for higher read/write throughput, lower latency, and acceptable tiered costs on the storage data layer. The training phase repeatedly reads samples and writes checkpoints, while inference emphasizes low-latency loading of model weights and intermediate states. Both workload types amplify demand for NVMe enterprise SSDs and high-speed NAND.

| Workload Type |

Core Storage Operations |

Latency Sensitivity |

Typical Storage Media |

| AI Training |

Dataset traversal, checkpoint writing |

Medium-High |

Enterprise NVMe SSD, parallel file system backends |

| AI Inference |

Model weight loading, intermediate state read/write |

High |

Low-latency SSD, near-compute cache |

| Data Preprocessing |

Batch transformation, feature engineering |

Medium |

High-speed SSD staging layer |

| Model & Log Archiving |

Long-term retention, low-frequency access |

Low |

HDD cold storage tier |

The increase in data layer demand does not guarantee proportional revenue growth for storage vendors. Customer procurement timing, inventory levels, industry capacity releases, and NAND price cycles all modulate actual SSD shipments and gross margins.

Enterprise SSD Scenarios in AI Infrastructure

In AI infrastructure, enterprise SSDs primarily serve the hot and warm data tiers, covering model weight storage, training checkpoints, dataset staging, intermediate file exchange for distributed training, and low-latency read paths for inference services. The SNDK business structure and product matrix breaks down SanDisk's product lines into enterprise, client, and embedded categories, with NVMe SSDs for data centers and cloud showing the strongest correlation to AI scenarios.

The hot data tier must keep the GPU queue saturated, while the warm data tier stores sub-high-frequency dataset shards or model versions. SanDisk enterprise SSDs enter AI clusters through cloud providers or server OEMs, with procurement involving performance qualification, endurance (DWPD), and total cost of ownership. When analyzing SNDK stock, the enterprise revenue share provides a more accurate gauge of actual exposure than an "AI concept" label.

How NAND Flash, HDD, and DRAM Divide the Roles in AI Storage

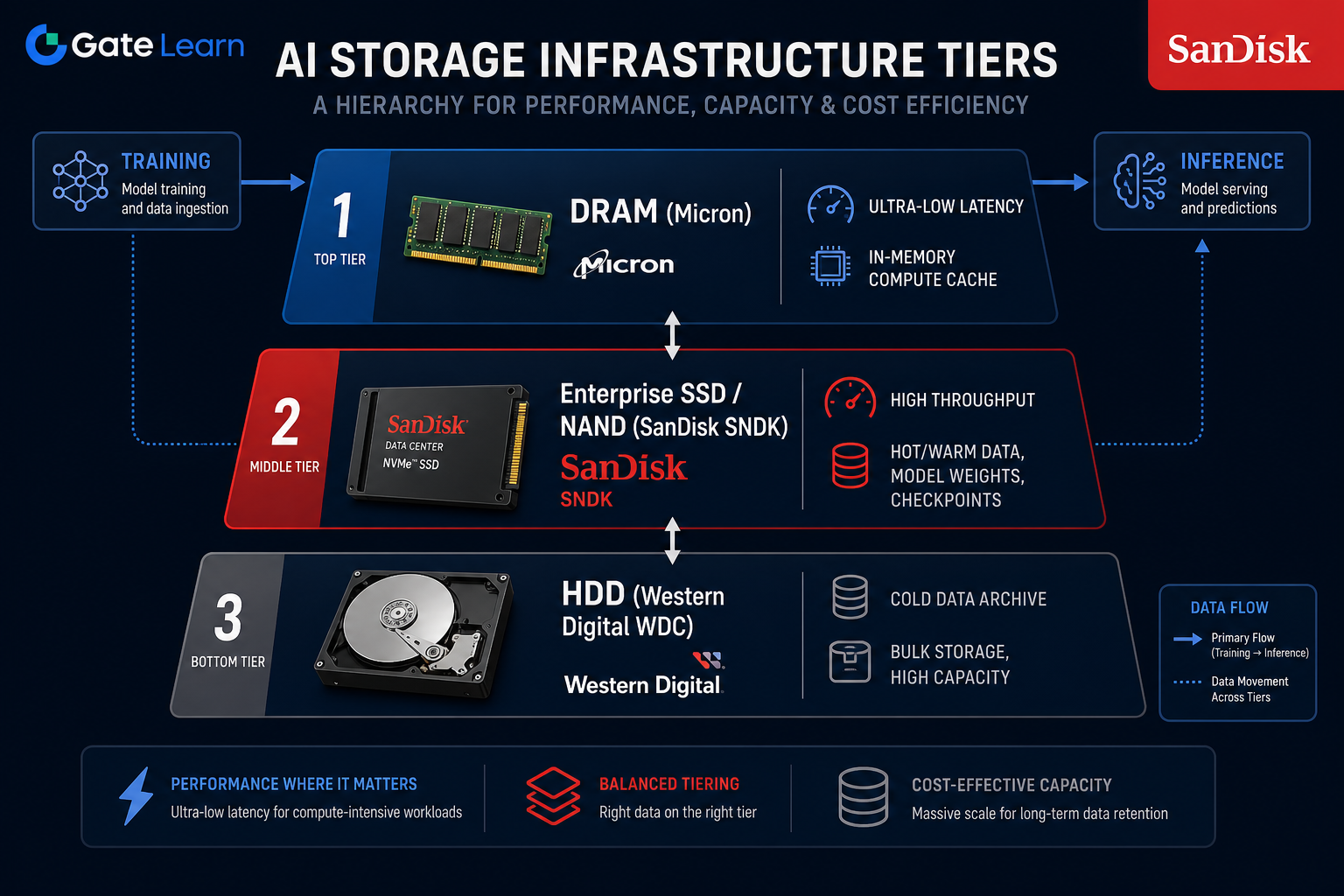

AI data center storage widely adopts a tiered architecture: DRAM handles in-memory computing and shortest-path caching, NAND Flash and enterprise SSDs handle high-speed read/write for hot and warm data, and HDDs handle cold data and large-scale archiving. These three media types complement each other in latency, cost per unit capacity, and endurance characteristics rather than serving as simple substitutes.

Western Digital (WDC) retains its HDD business after the spin-off, with mechanical hard drives suitable for high-capacity, low-cost archiving. Micron's DRAM and HBM provide the highest-bandwidth cache for GPU near-compute operations, operating in a different segment from NAND. SNDK's NAND and SSD tier sits between DRAM and HDD, ideal for carrying hot/warm data blocks that cannot fully fit into memory. SNDK vs WDC vs Micron offers a horizontal comparison from business purity and cyclical variable perspectives.

Figure 1. AI storage tier architecture: DRAM (Micron) handles memory cache, enterprise SSD/NAND (SNDK) covers hot/warm data, HDD (WDC) focuses on cold data archiving.

Figure 1. AI storage tier architecture: DRAM (Micron) handles memory cache, enterprise SSD/NAND (SNDK) covers hot/warm data, HDD (WDC) focuses on cold data archiving.

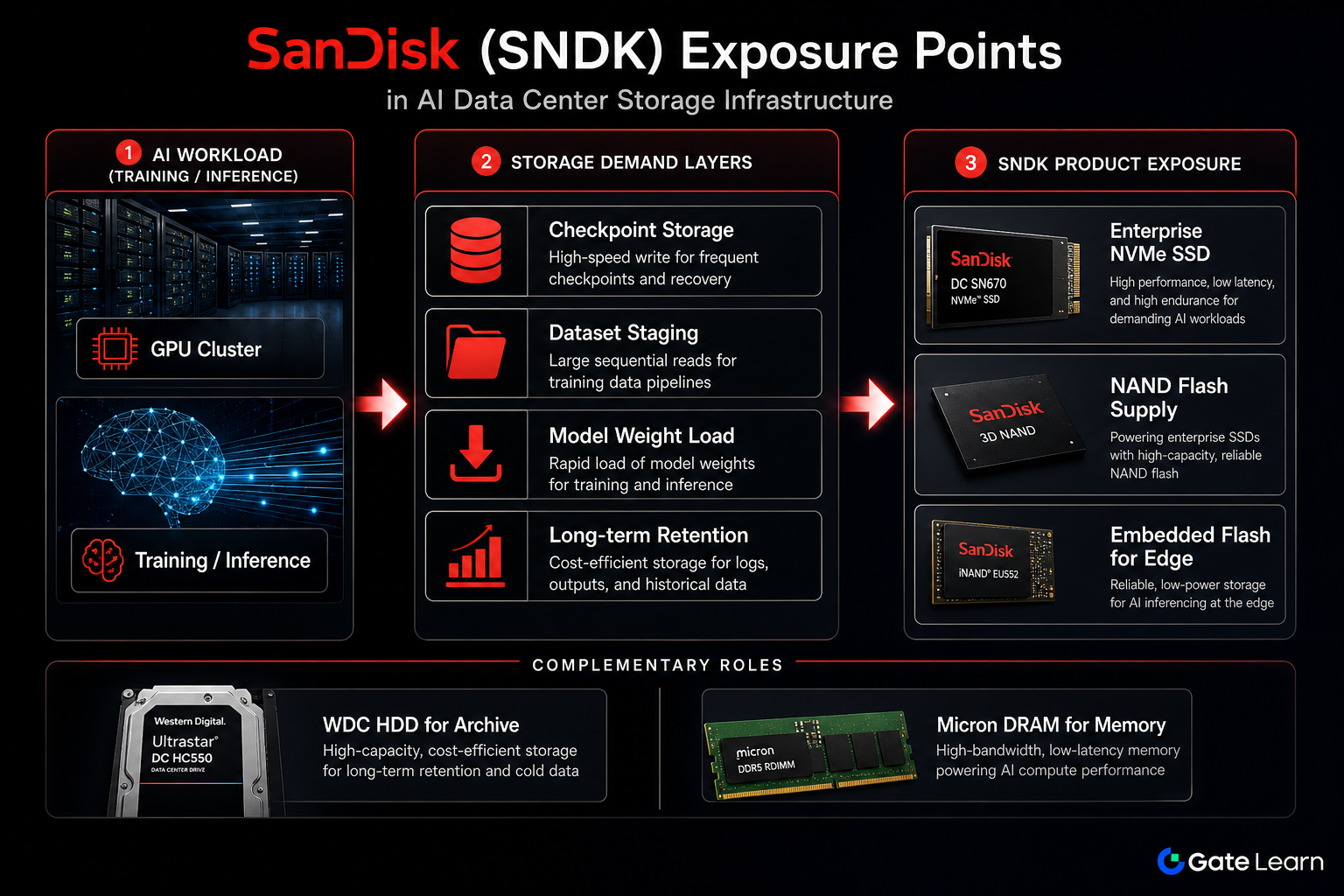

SNDK Stock Exposure Points in the AI Storage Chain

SNDK's exposure is concentrated in NAND Flash supply, enterprise SSD shipments, and data center certification share. AI infrastructure expansion drives SSD demand, but capacity utilization, competitive supply, and customer inventory simultaneously affect average selling prices and shipments. This must be assessed alongside enterprise revenue metrics in financial reports and should not be modeled independently of NAND cycles.

| Exposure Dimension |

Business Vehicle |

AI Scenario Relevance |

Primary Volatility Source |

| Chip Layer |

NAND Flash wafers |

Cost basis for SSD & embedded solutions |

NAND ASP, capacity utilization |

| Product Layer |

Enterprise NVMe SSD |

Training checkpoints, inference weight loading |

Cloud capex, certification share |

| Customer Layer |

Cloud providers & OEMs |

AI cluster storage expansion |

Procurement pace, inventory cycles |

| Competitive Layer |

Global flash memory landscape |

High-end SSD specification race |

Process technology, yield, price competition |

Figure 2. SNDK's exposure path in AI data centers: mapping from training and inference workloads to enterprise SSD and NAND Flash supply.

Figure 2. SNDK's exposure path in AI data centers: mapping from training and inference workloads to enterprise SSD and NAND Flash supply.

How AI Demand, NAND Cycles, and Capacity Transmit to SNDK

AI demand affects SNDK through a chain of "shipment pull → price transmission → gross margin fluctuation," which is not a linear one-way relationship. Cloud capex expansion can improve SSD shipments, but chip ASP declines during NAND expansion cycles may still compress gross margins. On the supply side, focus on wafer starts and capital expenditure; on the demand side, monitor cloud inventory and server shipments. When the two sides diverge, SNDK profitability must be measured by financial indicators. The SNDK key metrics and risk checklist organizes gross margin, inventory turnover, and capacity utilization into verifiable observation items. AI demand combines with traditional NAND downstreams like PCs and smartphones to form the demand mix; no single theme covers all cyclical variables.

Key Notes for Analyzing SNDK and AI Storage

When correlating SNDK with AI storage, note the following: AI investment does not equate to proportional revenue growth; "AI storage" spans multiple technology layers including DRAM, HBM, SSD, and HDD, with SNDK only covering the NAND and SSD subset; under strong NAND cyclicality, shipments must be distinguished from profitability; post-spin-off, use SNDK's standalone disclosure data, not commingled WDC historical figures. SNDK has pure NAND exposure and clear technology tier positioning, but faces risks from price cycles, competition, and customer concentration. These factors do not constitute a buy or sell judgment.

Summary

SanDisk (SNDK) plays the role of NAND Flash and enterprise SSD supplier in AI storage infrastructure, serving the hot and warm data tier for training and inference scenarios. Western Digital (WDC)'s HDDs and Micron's DRAM form complementary roles in cold archive and memory cache layers, respectively. SNDK's financial performance as a US-listed stock is jointly driven by AI demand, enterprise SSD shipments, and NAND price cycles. Analysis must incorporate capacity, inventory, and competitive landscape, avoiding the simplistic equation of the AI theme with a unidirectional positive outlook.

FAQ

What storage products does SNDK provide in AI data centers?

SNDK supplies high-speed solid-state storage for AI training and inference infrastructure through enterprise NVMe SSDs and underlying NAND Flash, commonly used for model weight storage, checkpoint read/write, and dataset staging in hot/warm data scenarios. Specific deployment configurations vary by customer architecture and OEM integration methods.

Does AI storage demand guarantee SNDK revenue growth?

Not necessarily. AI demand can drive enterprise SSD procurement, but NAND price cycles, industry capacity, customer inventory, and competitive share simultaneously affect SNDK's revenue and gross margins. Demand narratives must be cross-validated with financial indicators and industry supply signals.

How do SNDK, WDC, and Micron differ in AI storage?

SNDK focuses on NAND Flash and enterprise SSDs, covering the high-speed hot/warm data layer; post-spin-off, WDC primarily deals in HDDs, focusing on cold data high-capacity archiving; Micron covers DRAM and HBM memory categories, handling the shortest-path cache on the computing side. These three have different technology trajectories and cyclical variables, corresponding to different US-listed stocks.

Priority metrics for researching SNDK and AI

Priority can be given to tracking NAND ASP and capacity utilization, enterprise SSD revenue share, gross margin and inventory turnover, capital expenditure pace, and major cloud customer procurement cycles. Metric verification frameworks can refer to content like the SNDK key metrics and risk checklist, and always rely on SNDK's independently disclosed financial reports.

Where does competition come from for SNDK in AI storage?

Competition arises from global NAND and SSD giants in enterprise specification, process cost, endurance certification, and delivery capability, including Samsung, SK Hynix, Micron, and others. Cloud customers' in-house or deeply customized storage solutions may also alter the share structure of third-party SSD suppliers.

What to confirm before trading SNDK on Gate

You can search the code SNDK on Gate Stocks, verify that the underlying corresponds to SanDisk Corporation (not Western Digital), and understand US stock trading fees, order rules, and fund settlement details.