The business structure of SanDisk (SNDK) stock is the foundation for understanding the financial reporting and industry cycles of this U.S.-listed equity. SNDK trades independently on Nasdaq under SanDisk Corporation, carrying the NAND Flash and SSD businesses spun off from Western Digital. This scope directly aligns with the pure flash positioning, NAND cycle exposure, and ticker differentiation from WDC highlighted in SanDisk (SNDK). The product matrix unfolds across four dimensions: consumer flash, enterprise cloud SSD, mobile and automotive flash, and the revenue transmission mechanism.

The storage industry splits into two major technology camps: HDD and Flash. SNDK stock is directly exposed to the NAND Flash price cycle and SSD demand fluctuations, now fully separated from Western Digital (WDC), which retains the HDD business. Investors must first clarify each SNDK product line's function, then cross-reference them with industry supply and downstream procurement trends.

From a trading perspective, SNDK is a U.S.-listed storage stock that can be traded with USDT on platforms like Gate Stocks. Its product structure and revenue mix determine the sensitivity of SNDK stock to NAND market conditions, cloud capital expenditure, and the terminal device replacement cycle.

What Is the Business Structure of SNDK Stock? A Comprehensive Breakdown

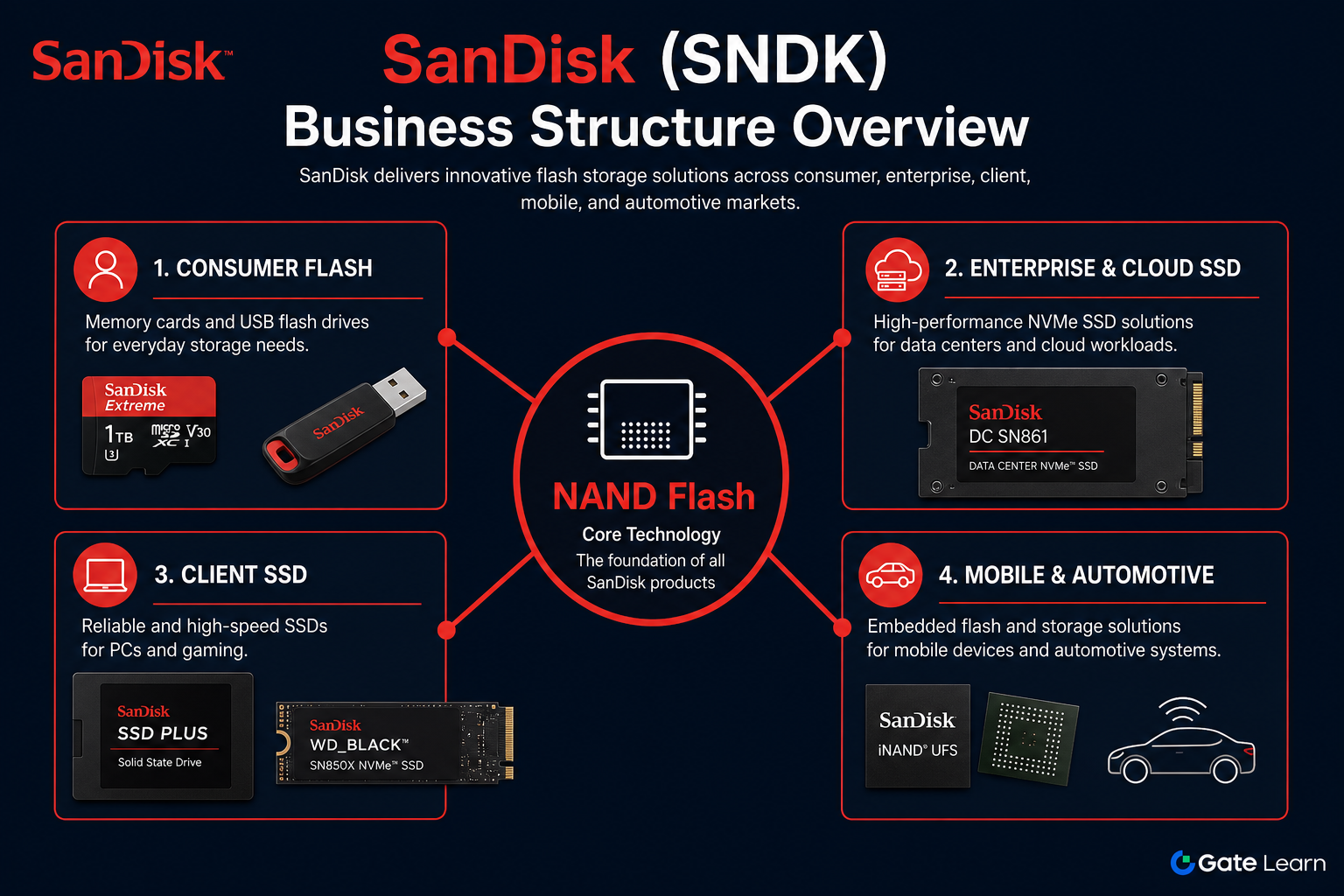

The business covered by SNDK stock is built on NAND Flash technology, integrating controller chips and firmware upstream, and delivering products downstream as SSDs, memory cards, USB drives, and embedded flash into consumer, enterprise, and automotive supply chains. The SanDisk brand enjoys longstanding recognition in consumer flash; post-spin-off, this brand is tied to the SNDK listed entity, while enterprise-grade SSDs target cloud providers and AI infrastructure operators.

SNDK's business can be summarized as "one technology layer, two types of integration, and four scenario groups": NAND Flash wafers are the common upstream; controllers and firmware complete chip-level integration; SSDs and embedded flash are the end-product delivery forms; consumer flash, enterprise cloud SSD, client SSD, and mobile/automotive flash constitute the four major downstream scenarios.

| Business Tier |

Core Component |

Function |

Corresponding Product Form |

| Upstream |

NAND Flash Wafer |

Memory cell manufacturing, process node iteration |

Internal wafer supply, sold chips |

| Midstream |

Controller and Firmware |

Read/write scheduling, error correction, performance optimization |

Various SSDs and embedded solutions |

| Downstream |

Standardized Storage Products |

Delivery to OEMs and channels |

Enterprise SSD, client SSD, memory card, automotive-grade flash |

NAND determines the cost curve and supply elasticity, while SSDs and embedded solutions determine the revenue mix and gross margin profile. Analyzing SNDK stock requires simultaneous tracking of wafer utilization and shipment proportion by category. The health of a single product line is insufficient to represent the company's overall performance.

Figure 1. SNDK Business Structure Overview: With NAND Flash at the core, extending to four categories: consumer flash, enterprise cloud SSD, client SSD, and mobile/automotive flash.

Figure 1. SNDK Business Structure Overview: With NAND Flash at the core, extending to four categories: consumer flash, enterprise cloud SSD, client SSD, and mobile/automotive flash.

What Product Lines Exist in Consumer Flash? How Do Memory Cards and Portable Storage Operate?

Consumer flash is the business segment with the highest brand recognition for SanDisk, covering SD cards, microSD cards, USB drives, and portable SSDs sold through retail and channels. This segment directly serves individuals and vertical markets such as photography, gaming, and drones. It is sensitive to NAND price movements, but channel stocking and brand premiums can partially mitigate chip cost volatility.

The operational logic of consumer flash: SNDK manufactures NAND chips, which are then packaged and integrated with a controller into memory cards or USB drives, reaching the end market through retail channels and OEM preinstallation. Product iteration revolves around capacity tiers, read/write speeds, and durability ratings. This segment typically carries lower gross margins than enterprise SSDs, but it provides stable cash flow and drives SanDisk brand visibility in the end market.

How Are Enterprise and Cloud SSDs Positioned? What Role Do Data Center Scenarios Play?

Enterprise and cloud SSDs are the higher-margin business segment for SNDK, serving hyper-scale cloud providers, AI infrastructure operators, and enterprise data centers. The product form is primarily NVME interface SSDs, emphasizing high IOPS, low latency, large capacity, and long-term reliability. They are commonly used for hot data caching, database acceleration, and high-speed storage layers in AI training clusters.

Enterprise SSDs require customer qualification and long-term supply agreements, with longer delivery cycles than consumer products. When cloud vendors expand capital expenditure, enterprise SSD procurement typically rises first; during downturns, both shipment volume and pricing come under pressure. SNDK's enterprise SSDs in AI data centers serve functions such as model weight loading and high-speed caching. SNDK and AI Storage Demand distinguishes the storage layering logic for training, inference, and edge scenarios. This segment features long qualification cycles and high customer concentration, making it a part of SNDK's revenue structure with both margin potential and volatility.

What Role Do Mobile and Automotive Flash Play? How Are Embedded Solutions Delivered?

Mobile and automotive flash are part of the embedded NAND Flash business, where chips are directly embedded into smartphones, tablets, wearables, and automotive electronic systems as modules or custom packages, bypassing retail channels. This segment's revenue correlates with global smartphone shipments, automotive electronics penetration, and automotive-grade certification progress.

Mobile embedded flash emphasizes small size and low power consumption; automotive flash must meet standards such as AEC-Q100, with long certification cycles, but once integrated into a vehicle platform, customer stickiness is high.

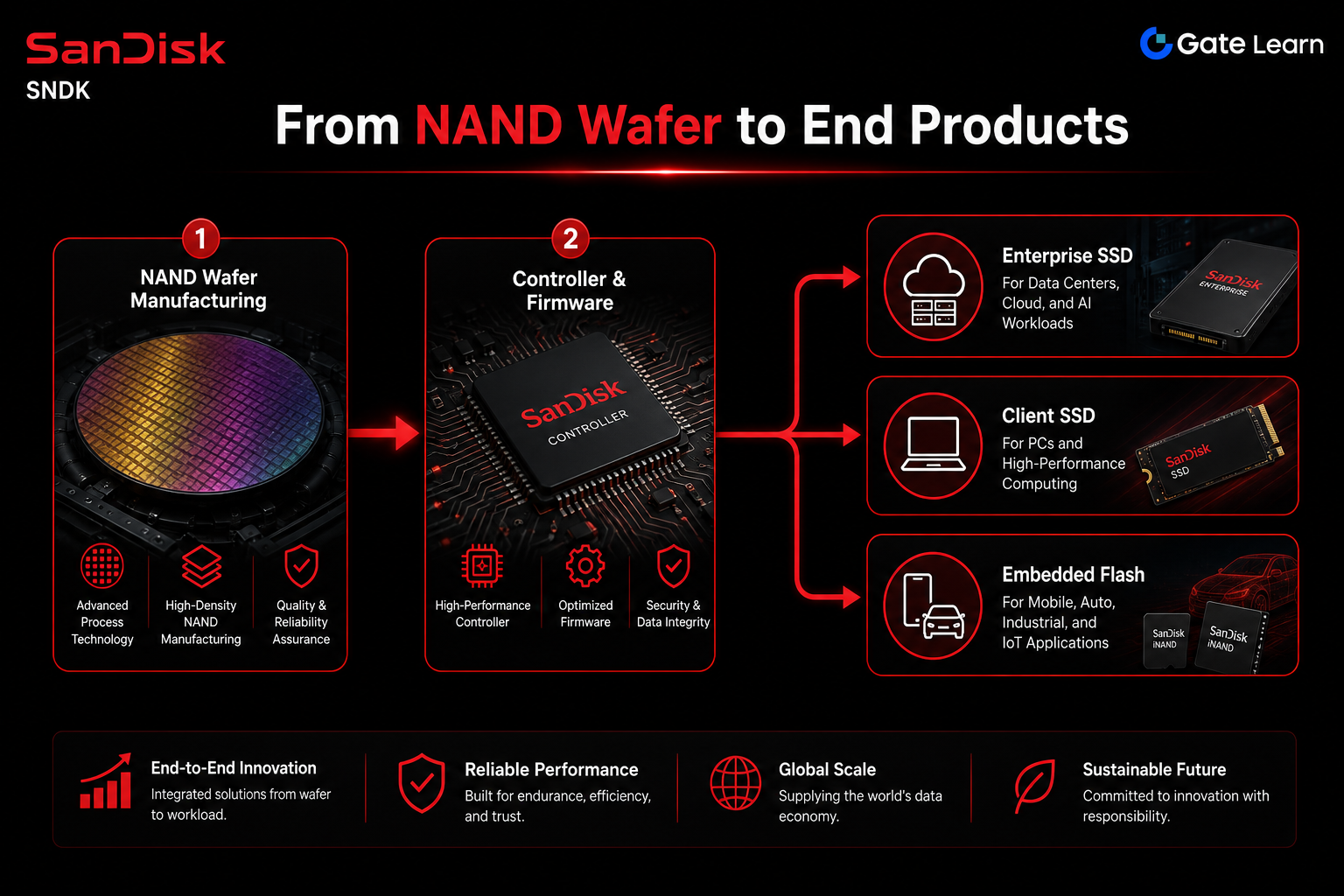

Figure 2. From NAND Wafer to End Products: After controller and firmware integration, products flow to three delivery paths: enterprise SSD, client SSD, and embedded flash (mobile/automotive).

Figure 2. From NAND Wafer to End Products: After controller and firmware integration, products flow to three delivery paths: enterprise SSD, client SSD, and embedded flash (mobile/automotive).

With automotive-grade flash growing alongside smart cockpit and autonomous driving demand, the cyclical rhythm of mobile and automotive segments is misaligned with consumer flash and enterprise SSDs, helping to diversify single-market fluctuations.

How Is SNDK Revenue Transmitted through NAND Prices and SSD Demand?

SNDK's revenue and profit margins transmit through the NAND Flash industry cycle via this path: wafer capital expenditure determines medium- to long-term supply → capacity release affects NAND average selling price → SSD and embedded product pricing adjusts with chip costs → shipment structure by category determines revenue mix → gross margins and operating cash flow fluctuate.

Supply-side signals include new capacity coming online, process node migration progress, and fab utilization rates; demand-side signals include cloud capital expenditure, PC replacement cycles, smartphone shipments, and automotive electronics penetration. Both signal types must be read together — a single NAND price indicator cannot capture the buffering or amplifying effects of SSD structural changes on revenue.

| Transmission Layer |

Supply-Side Variables |

Demand-Side Variables |

Impact on SNDK |

| NAND Chip Layer |

Capacity, process node, utilization |

Inventory destocking speed |

Directly determines chip business gross margin |

| Enterprise SSD Layer |

Product qualification cycle |

Cloud CAPEX, AI cluster expansion |

Affects revenue share of high-margin products |

| Consumer Flash Layer |

Channel stocking strategy |

Promotional pace, seasonal demand |

Affects shipment volume and average selling price mix |

| Embedded Layer |

Automotive qualification progress |

Smartphone shipments, automotive electronics adoption |

Affects medium- to long-term order visibility |

SNDK Core Metrics and Risk Checklist organizes indicators such as gross margin, inventory turnover, capital expenditure, and capacity utilization into a checkable observation framework. Cycle assessment must combine supply-side and demand-side signals, avoiding directional inferences based solely on NAND spot prices.

Where Is the Business Boundary between SNDK and WDC? Why Must They Be Analyzed Separately?

After the 2025 spin-off, SNDK and Western Digital (WDC) became two independent public companies, with the business boundary drawn along technology lines: WDC retains HDD hard disk storage, while SNDK takes all NAND Flash and SSD flash memory businesses. SanDisk Spin-Off and WDC/SNDK Relationship outlines the spin-off timeline, shareholder distribution, and ticker identification details.

HDD suits large-capacity archiving, while NAND Flash and SSD suit low-latency and mobile scenarios. Post-spin-off, investors can use the SNDK ticker to track the flash cycle separately and the WDC ticker to track the hard disk cycle. SNDK vs WDC vs Micron provides a horizontal comparison across business purity, cycle exposure, and financial reporting. When researching SNDK stock, financial statements must be searched using SNDK as the entry point and must not be conflated with WDC's HDD reporting.

Conclusion

SNDK stock corresponds to SanDisk Corporation. Its business is built on NAND Flash as the underlying technology. After controller and firmware integration, it delivers products across four categories: consumer flash, enterprise cloud SSD, client SSD, and mobile/automotive embedded flash. Revenue is jointly driven by NAND prices, shipment structure by category, and capital expenditure cycles. It is completely separated from WDC, which retains HDD, in both technology and cycles. Understanding the product matrix is a prerequisite for analyzing SNDK's financial performance and industry positioning.

FAQ

What is the core business of SNDK stock?

SNDK stock corresponds to SanDisk Corporation. Its core business is NAND Flash manufacturing and product delivery primarily through SSDs, memory cards, USB drives, and embedded flash, covering four scenarios: consumer, enterprise cloud, client, and mobile/automotive.

What is the difference between SNDK consumer flash and enterprise SSDs?

Consumer flash targets retail and channels with products including SD cards, USB drives, and portable SSDs. It is sensitive to NAND prices and has relatively lower gross margins. Enterprise SSDs target cloud providers and data centers, require long-term qualification, emphasize high IOPS and reliability, and typically have higher gross margins and longer order cycles.

What cyclical factors primarily affect SNDK revenue?

SNDK revenue is mainly affected by NAND Flash average selling price, wafer capacity utilization, enterprise and client SSD shipment volumes, cloud capital expenditure pace, and the storage industry capital expenditure cycle. Supply-side and demand-side signals must be read together.

How is the business boundary between SNDK and WDC defined?

Post-spin-off, SNDK operates all NAND Flash and SSD businesses, while WDC retains the HDD hard disk business. Both companies are independently listed and disclose financials separately. Financial data must be searched using the SNDK and WDC tickers respectively and should not be read from combined reports.

What storage products does SNDK provide in AI data centers?

SNDK provides high-speed solid-state storage layers for AI training and inference infrastructure through enterprise NVMe SSDs, commonly used for hot data caching, model weight loading, and intermediate result storage. Specific deployment layering varies by customer architecture.

Factors to watch include: the transmission of NAND price volatility to gross margins across product categories, enterprise customer concentration, automotive certification and supply stability, cost pressure from process node competition, and the impact of post-spin-off independent operational scale and industry capacity releases on shipments. Financial analysis should use SNDK's independently disclosed data.