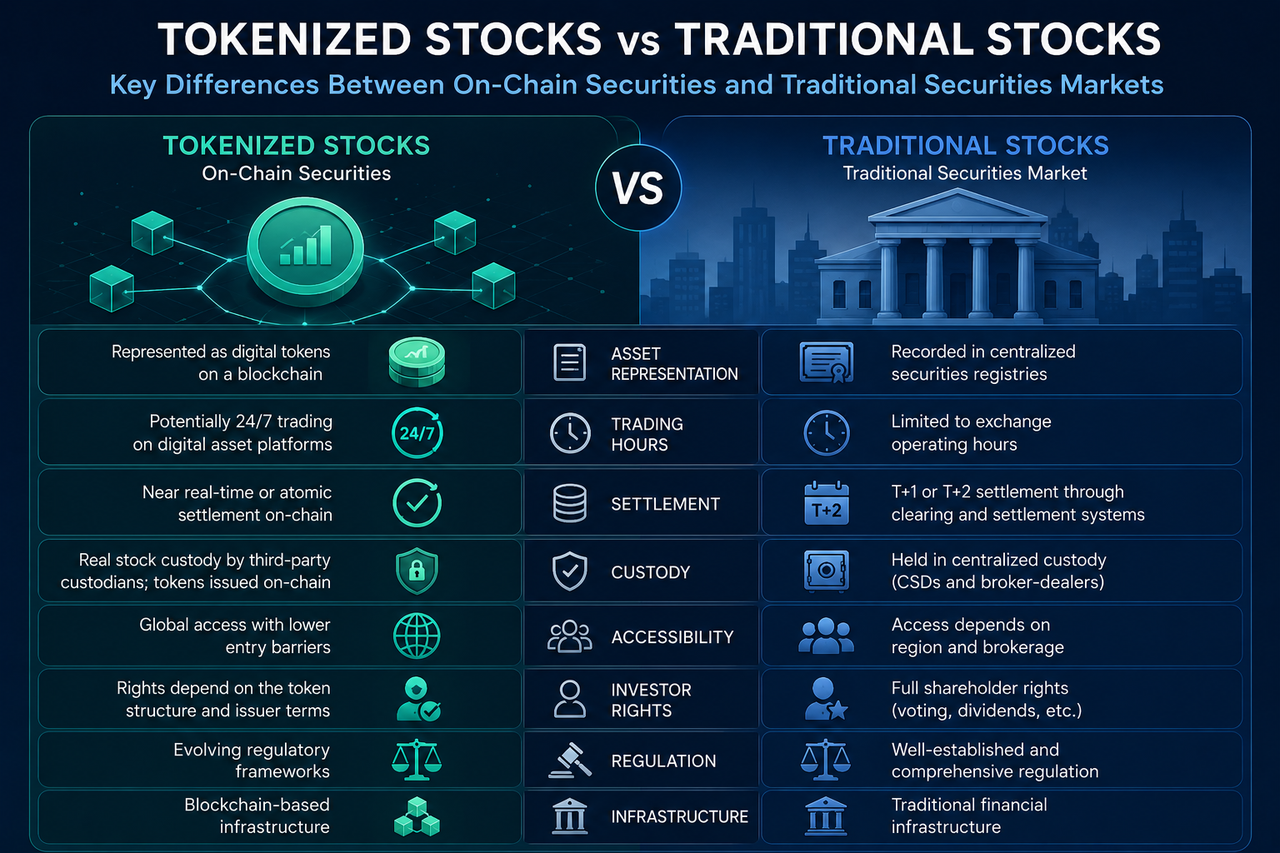

Tokenized stocks are a form of digital securities that map real-world stock assets onto blockchain networks, while traditional stocks are financial assets issued and circulated through securities exchanges and central securities registration systems. Although both are connected to listed company shares, the operating logic and infrastructure behind them are not the same.

As the tokenization of real-world assets, or RWA, continues to develop, tokenized stocks are gradually becoming an important direction in the convergence of traditional finance and digital assets. As one of the most representative asset categories in the RWA sector, tokenized stocks are helping extend equity assets from the traditional securities system into on-chain financial infrastructure.

What Are Tokenized Stocks?

Tokenized stocks are a form of on-chain digital asset created by using blockchain technology to represent real-world shares. Their value is usually linked to the corresponding stock, and they are held and traded in the form of digital tokens.

In most models, the issuer first purchases and custodies the actual shares, then issues a corresponding number of on-chain tokens according to a set ratio. What investors actually hold is a digital certificate, while the underlying shares are managed by a custodian.

Tokenized stocks are an important part of real-world asset tokenization and also represent a major attempt to connect blockchain with traditional securities markets.

What Are Traditional Stocks?

Traditional stocks are ownership certificates issued by listed companies. They represent an investor’s partial ownership of a company and the related rights that come with it.

In traditional securities markets, stock trading usually depends on securities exchanges, brokers, central securities depositories, and clearing institutions working together. Investors buy and sell stocks through securities accounts, while ownership records are maintained by a centralized registration system.

After decades of development, traditional stock markets have built mature regulatory frameworks, trading mechanisms, and investor protection systems, making them an important part of global capital markets.

How Do the Two Types of Stocks Differ in Asset Structure?

The core difference between tokenized stocks and traditional stocks comes from the way the asset is represented.

Traditional stocks are recorded directly within a securities registration system, and investors hold shares in their securities accounts. Tokenized stocks, by contrast, exist as digital tokens on a blockchain network, and investors hold the corresponding assets through digital asset wallets or platform accounts.

In terms of value source, both are related to listed company shares. However, tokenized stocks add extra layers, including the issuer, custodian, and on-chain issuance structure.

In this sense, tokenized stocks essentially add a digital mapping mechanism on top of traditional shares.

How Are the Trading Methods Different?

Traditional stock trading mainly takes place during the opening hours of securities exchanges.

Investors need to submit orders through brokers, and exchanges are responsible for matching those orders. The trading process is affected by market hours and regional regulatory rules.

Tokenized stocks, on the other hand, operate on digital asset platforms and blockchain networks.

Because blockchain infrastructure usually runs around the clock, some tokenized stock products can support extended trading hours or even near 24-hour trading. Users can buy and sell through digital asset accounts without relying on the traditional securities account system.

This difference creates a clear gap between the two in terms of market accessibility.

Why Are the Settlement Mechanisms Different?

Settlement is one of the areas where the difference between tokenized stocks and traditional stocks is most obvious.

Traditional securities markets usually use a T+1 or T+2 settlement model. After a trade is completed, a clearing institution still needs to calculate the delivery results, and a central securities depository completes the final registration.

Tokenized stocks can use a blockchain ledger to record asset transfers directly.

In some models, trade confirmation and asset settlement can be completed almost at the same time. This is often referred to as atomic settlement, which can reduce the time costs and counterparty risks caused by intermediary steps.

For this reason, blockchain is seen as having the potential to improve settlement efficiency in securities markets.

How Do the Custody Systems Differ?

Traditional stock markets use a mature central custody system.

Although investors hold stocks through brokers, the final registration and management of assets are handled by central securities depositories. Regulators can also supervise and manage the entire market in a unified way.

Tokenized stocks usually follow a model of “real stock custody plus on-chain token issuance.”

The underlying shares are held by professional custodians, while the on-chain tokens are issued and managed by the issuer. As a result, investors need to pay attention not only to the stock itself, but also to the operations of the issuer and the custodian.

This structure gives tokenized stocks greater flexibility, but it also introduces additional custody risks.

Are Investor Rights Exactly the Same?

Tokenized stocks and traditional stocks are not necessarily identical in terms of investor rights.

Traditional stocks usually grant investors clear shareholder rights, including voting rights, the right to attend shareholder meetings, and the right to receive dividends.

Whether tokenized stocks offer the same rights depends on the specific product design.

Some tokenized stocks provide only price-related economic exposure and do not include full shareholder rights. Other products may map rights such as dividends to on-chain tokens through their issuance structure.

Therefore, understanding the specific product terms is very important when assessing investor rights.

How Do the Regulatory Frameworks Differ?

Traditional stock markets have mature and clearly defined regulatory systems.

Securities issuance, trading, custody, and information disclosure are all subject to strict supervision by regulators. The rights and responsibilities of market participants also have a relatively complete legal foundation.

Tokenized stocks, by contrast, are still in a stage of regulatory exploration.

Different countries and regions do not have a unified legal definition for digital securities and tokenized stocks. Some jurisdictions have already established regulatory frameworks for digital securities, while others are still studying the relevant rules.

Regulatory differences are one of the main challenges facing the development of the tokenized stock market today.

Tokenized Stocks vs Traditional Stocks

| Comparison Dimension |

Tokenized Stocks |

Traditional Stocks |

| Asset Form |

On-chain digital tokens |

Securities registration records |

| Holding Method |

Digital asset account or wallet |

Securities account |

| Trading Hours |

May support round-the-clock trading |

Exchange opening hours |

| Settlement Mechanism |

Real-time or near real-time on-chain settlement |

T+1 or T+2 |

| Custody Model |

Stock custody plus token issuance |

Central securities depository |

| Circulation Scope |

Global digital asset market |

Regional securities market |

| Technical Architecture |

Blockchain network |

Traditional financial infrastructure |

| Regulatory Maturity |

Developing stage |

Highly mature |

| Investor Rights |

Depends on product structure |

Clearly defined rights |

Conclusion

Tokenized stocks and traditional stocks are both connected to the value of listed company shares, but they are built on different infrastructure. Traditional stocks rely on securities exchanges, brokers, and central securities depositories, while tokenized stocks use blockchain networks to record and circulate assets.

The two differ significantly in asset structure, trading methods, settlement efficiency, custody models, investor rights, regulatory frameworks, and other areas.

FAQs

Are Tokenized Stocks the Same as Holding Real Stocks?

Not necessarily. Some tokenized stocks are backed 1:1 by real shares, while other products only provide price exposure. Investors need to review the specific issuance structure and product description.

Why Is Settlement Faster for Tokenized Stocks?

Tokenized stocks can use blockchain to directly record asset transfers and ownership changes, reducing the clearing and registration steps found in traditional securities markets and improving settlement efficiency.

Why Is Regulation More Mature for Traditional Stocks?

Traditional stock markets have developed over a long period of time and have established complete legal systems, regulatory frameworks, and investor protection mechanisms. As a result, their regulatory maturity is usually higher than that of tokenized stock markets.

Do Tokenized Stocks Have Shareholder Voting Rights?

Not all tokenized stocks grant full shareholder rights. Some products provide only economic rights, and whether voting rights are included depends on the issuance structure and product design.

Will Tokenized Stocks Replace Traditional Stocks?

At present, the two are more likely to coexist over the long term. Traditional stock markets have mature infrastructure, while tokenized stocks offer a new technical path and method of circulation. In the future, they may develop a complementary relationship.