Image Source: Kinetiq Official Website

Image Source: Kinetiq Official Website

Unlike the traditional "staking equals locking" model, Kinetiq directly resolves the structural tension between staking yield and capital efficiency on Hyperliquid — a high-performance on-chain trading and DPoS network. When large amounts of HYPE are natively staked, they become illiquid and cannot participate in the fast-growing DeFi ecosystem on HyperEVM. When left unstaked, network security and long-term returns suffer. Liquid staking separates staking rights from liquidity and tokenizes them, making it a standard financial middleware layer in mature L1 ecosystems.

From an infrastructure standpoint, Kinetiq bridges Hyperliquid L1 consensus security with the HyperEVM application layer: it pools HYPE on one side and delegates to validators, while minting the standard ERC-20 asset kHYPE on the other side for use in lending, CDPs, yield vaults, and the HIP-3 market. The sections below cover project background, KNTQ tokenomics, the StakeHub mechanism, DeFi use cases, yield and risks, and ecosystem outlook — providing a comprehensive framework for evaluating Hyperliquid staking and KNTQ's value proposition.

What Is Kinetiq (KNTQ)? Project Background and Key Milestones

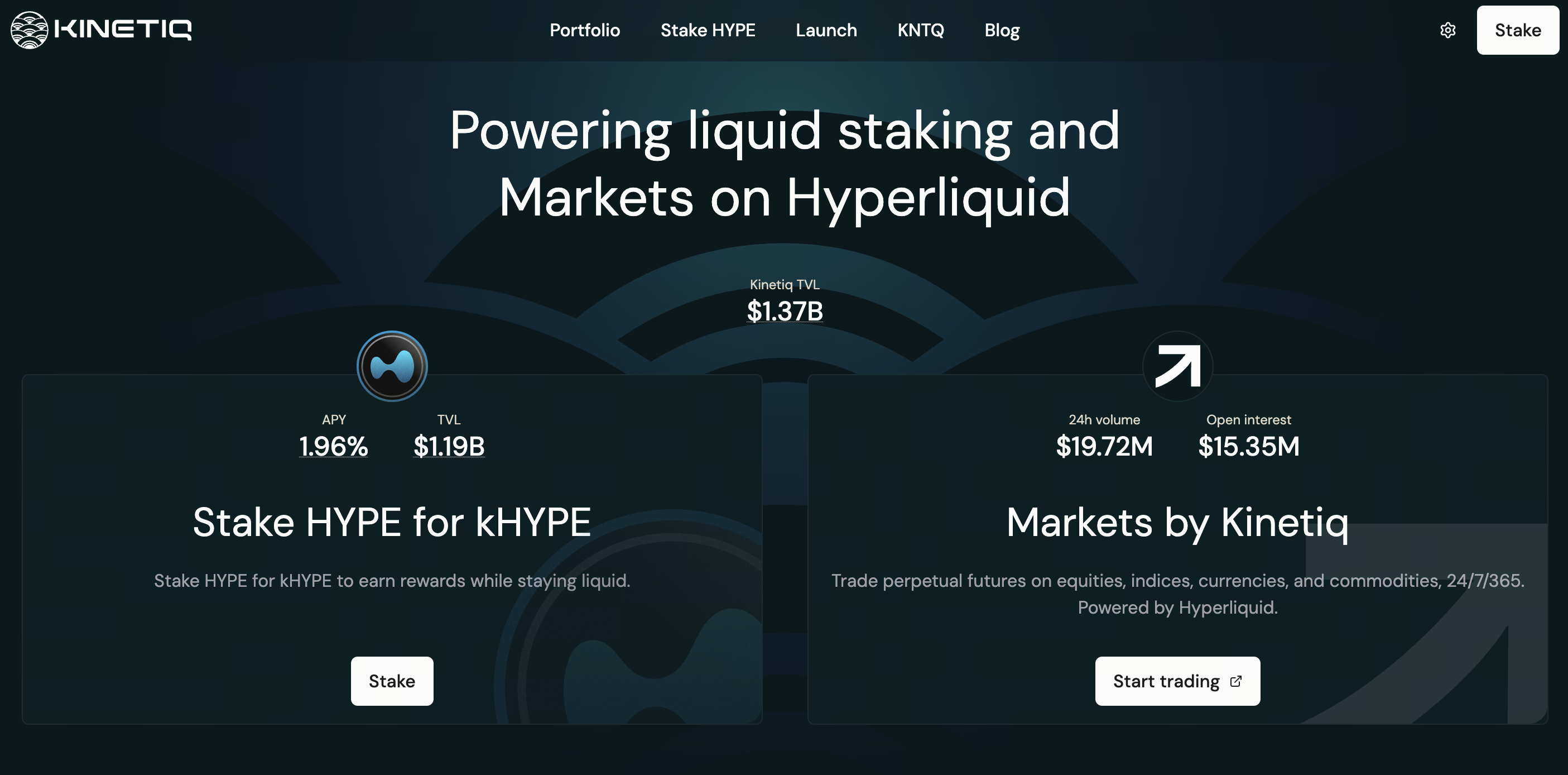

Founded in late 2024, Kinetiq raised approximately $1.75 million in early-stage funding and went live on mainnet on July 15, 2025. It ranks among the largest native liquid staking protocols on HyperEVM, with a peak TVL near $2.6 billion and a longstanding market share exceeding 80% in Hyperliquid liquid staking.

The product is built around kHYPE, with subsequent launches including Markets by Kinetiq (HIP-3 on-chain perpetuals, linked to kmHYPE), Kinetiq Earn yield vaults, institutional-grade iHYPE, and the KNTQ genesis distribution on November 27, 2025 — a landmark native token event in the Hyperliquid ecosystem. In January 2026, the sKNTQ module went live following a Spearbit audit. As of the first half of 2026, TVL has receded from its peak (approximately $780 million per DeFiLlama), though the protocol remains the dominant source of kHYPE liquidity. Starting April 9, 2026, a 10% performance fee is charged on staking rewards, with 70% allocated to KNTQ buybacks. Core contracts have been audited by Spearbit, Zenith, Pashov, and Code4rena, and are safeguarded by multi-signature wallets, emergency pause mechanisms, and Hypernative monitoring. For Hyperliquid users, Kinetiq has become one of the most common on-ramps for staking HYPE.

KNTQ Tokenomics and Value Capture Mechanism

KNTQ has a maximum supply of 1 billion tokens, officially defined by the team as the "sole instrument" for protocol value accrual. Allocation breakdown: 25% airdrop, 30% protocol growth, 23.5% core contributors, 10% foundation, 7.5% investors, 4% liquidity. Team and investor tokens follow a 3-year unlock schedule (1-year cliff + 2-year linear release).

| Mechanism |

Description |

| Revenue Buyback |

70% of protocol revenue (including 10% staking performance fee) is used to buy back KNTQ; 30% flows to the treasury |

| Validator Commission |

Active Set validators remit 50% of commissions earned from protocol delegation, with 100% of that amount used for buybacks |

| Trading Fee Burn |

100% of KNTQ trading fees go to the assistance fund, functioning as an equivalent burn |

| sKNTQ Distribution |

Buyback KNTQ is distributed to sKNTQ holders proportionally to their stake |

Staking KNTQ yields sKNTQ, unlocking tiered benefits including Markets referral fees (up to approximately 15%), fee discounts (up to approximately 30%), and kmHYPE minting quotas. This gives the token both governance rights and a "member profit-sharing" dynamic.

How Kinetiq Builds the Hyperliquid Liquid Staking Infrastructure

Hyperliquid uses DPoS, and native staking comes with lock-up periods, high costs for selecting validators, and limited DeFi composability. Kinetiq operates across L1 and HyperEVM: users deposit HYPE into the StakingManager, mint kHYPE at the current kHYPE:HYPE exchange rate, while the underlying StakeHub delegated to high-scoring validators.

Yields are reflected through "exchange rate appreciation" — the amount of kHYPE in a wallet remains constant, while each kHYPE becomes redeemable for more HYPE, avoiding the accounting complexities of rebasing in DeFi. The minimum direct stake is 5 HYPE; users with less can acquire kHYPE via a DEX. The unstaking queue takes approximately 8–9 days with a 0.10% fee; unstaking is not permitted within the first 24 hours of a stake, and tokens in the queue do not accrue rewards. kHYPE can also be sold immediately on the secondary market.

How kHYPE, sKNTQ, and the StakeHub System Work

kHYPE (Kinetiq Staked HYPE) represents a proportional share of the staking pool and accumulated rewards, with no manual claim required and an exchange rate updated daily — functionally similar to stETH's share-based LST model. The ecosystem also includes wrapper formats like wstHYPE to simplify integration with certain protocols.

StakeHub scores validators on a 0–100 scale across five dimensions: reliability, security, economics, governance, and longevity, and continuously rebalances delegations. Data is on-chain and publicly accessible, enabling use by third-party staking interfaces or novel LST designs. Users cannot manually select validators, trading direct control for automation and diversification, while relying on algorithmic and governance quality. The official FAQ notes that although Hyperliquid has not yet enabled slashing, if slashing is introduced in the future and a delegated validator violates rules, the kHYPE exchange rate could be affected. StakeHub's security dimension score is specifically designed to mitigate such tail risks.

sKNTQ is tied to protocol commercial revenue and the buyback/burn narrative, creating a two-layer structure with kHYPE — which tracks HYPE rewards — combining "underlying staking yield + protocol profit-sharing."

Kinetiq Use Cases in DeFi and the HyperEVM Ecosystem

kHYPE's value lies in its composability: it can serve as lending collateral, for DEX market-making, deposited into Kinetiq Earn for passive strategies, used as margin for Markets or third-party perpetuals, and to attract institutional capital via iHYPE. Some DeFi protocols accept both kHYPE and wstHYPE as collateral, with both deriving underlying yield from HYPE staking — the differences are primarily in token standards and integration preferences. As CDPs and yield trading (PT/YT) develop on HyperEVM, kHYPE is well-positioned to become the default "interest-bearing native asset." If competing protocols divert liquidity, the secondary market price may temporarily deviate from the redemption value, with arbitrageurs and LP depth determining the speed of convergence.

Analysis of Kinetiq's Yield Mechanism and Liquid Staking Model

User yield comes in two layers:

- The kHYPE-to-HYPE exchange rate rises, reflecting validator rewards, with APY fluctuating based on the network-wide staking rate and validator performance;

- Deploying kHYPE into lending, LP pools, or Earn pursues additional yield at added risk.

Protocol revenue drives KNTQ buybacks: the 0.10% unstaking fee, 10% performance fee (70% allocated to buybacks), Markets fees, and validator commissions. Native staking retains 100% of validator rewards with no protocol fees, but sacrifices liquidity — using Kinetiq effectively means paying a fee for the "liquidity premium."

How Kinetiq Differs from Other Liquid Staking Protocols

| Dimension |

Kinetiq |

Common Counterpart |

| Ecosystem Position |

Leads in TVL and integrations |

Competitors may have lower fees, but few match kHYPE's depth |

| Yield Model |

Exchange rate appreciation, non-rebasing |

Some use rebase or dual-token models |

| Validators |

StakeHub fully automated |

Native or some LSTs allow self-selection |

| Token Model |

KNTQ/sKNTQ + buybacks |

Many LSTs lack strong buyback mechanisms |

| Product Line |

Staking + Perpetuals + Vaults + Institutional |

Competitors often offer only LST |

Compared to Ethereum's Lido and Rocket Pool, Kinetiq is deeply tied to a single high-performance L1, concentrating benefits while also bearing chain-specific narrative risk.

Key Risks to Consider When Investing in KNTQ

- Market Risk: KNTQ is correlated with HYPE and ecosystem sentiment; a TVL decline weakens the leader narrative and buyback scale.

- Supply Risk: Token unlocks create selling pressure; declining revenue weakens the buyback narrative.

- Contract and Composability Risk: Audits cannot eliminate upgrade risks or risks from DeFi stacking.

- Validator Risk: Hyperliquid may introduce slashing in the future, potentially impacting the kHYPE exchange rate.

- Liquidity Risk: DEX discounts, an 8–9 day unstaking queue with no rewards during the waiting period.

- Regulatory and Governance Risk: Risks related to Markets, institutional products, fee changes, and buyback parameter modifications.

The above does not constitute investment advice.

Future Development Direction and Market Potential of the Kinetiq Ecosystem

Short-term growth depends on Hyperliquid trading volume, the HYPE staking rate, and the total size of HyperEVM DeFi. sKNTQ's tiered benefits (fee discounts, referral fees, kmHYPE quotas) help retain long-term users and boost Markets liquidity. In the medium term, Kinetiq may deepen StakeHub's role as an ecosystem public data layer, expand the iHYPE institutional channel and Earn strategy integrations, and enable HIP-3 deployers to create customized LSTs through pooled crowdfunding via Launch. The long-term outcome hinges on Hyperliquid's competitiveness in the on-chain derivatives sector, whether liquid staking becomes the default HYPE configuration, and the sustainability of revenue alongside governance decentralization. The KNTQ "real yield" narrative must be cross-verified through on-chain buyback addresses, sKNTQ profit-sharing, and TVL trends — not measured by market cap alone.

Summary

Kinetiq connects HYPE staking with DeFi liquidity: kHYPE preserves yield and composability, StakeHub simplifies delegation, and KNTQ/sKNTQ ties protocol revenue to product benefits. Evaluation should focus concurrently on the kHYPE exchange rate, TVL, validator quality, the performance fee and buyback mechanism, and the KNTQ unlock schedule. Before participating in staking or holding tokens, users should consult official documentation and on-chain real-time data, and independently assess risk and reward.

FAQs

What is the relationship between Kinetiq and Hyperliquid?

Kinetiq is a third-party liquid staking protocol built on Hyperliquid, utilizing L1 staking and HyperEVM contracts. It is not an official core chain component.

Which offers higher yield: kHYPE or directly staking HYPE?

Direct staking avoids the 10% performance fee and 0.10% unstaking fee, but locks up capital. kHYPE is suitable for those needing liquidity or DeFi composability; net yield depends on the combined fees and strategy risk.

What is the difference between KNTQ and sKNTQ?

KNTQ is a tradable governance token. sKNTQ is a staking receipt used for buyback distribution, fee discounts, and rights like kmHYPE.

How long does it take to unstake kHYPE?

The protocol queue takes approximately 8–9 days (0.10% fee, no rewards during the queue). It can also be traded instantly on DEX, but watch for slippage and discounts.

Where do KNTQ buyback funds come from?

70% of protocol revenue, 100% of validator remitted commissions, and KNTQ trading fee burns. Proceeds are distributed to sKNTQ holders.

Which validators does StakeHub select?

Validators are continuously scored on reliability, security, economics, governance, and longevity, with weight directed toward high-scoring validators. Users cannot manually specify validators.

Is it safe to participate in Kinetiq now?

It has passed multiple audits and is equipped with multi-signature and pause mechanisms. However, contract, future slashing, DeFi composability, and market risks remain. The official documentation states there is currently no dedicated insurance — users must evaluate independently.