As of the public fundraising disclosures in May 2026, Anthropic completed a $65 billion Series H round, pushing its post-money valuation to $965 billion. OpenAI secured $122 billion in March 2026, resulting in a post-money valuation of $852 billion. Anthropic’s current valuation exceeds OpenAI’s by roughly $113 billion. However, this difference does not necessarily indicate that Anthropic leads OpenAI across all metrics such as user base, revenue quality, or long-term value.

Private company fundraising valuations are not the same as the real-time market caps of public companies. These valuations are determined by the latest funding price, investor terms, share classes, and market expectations. Thus, when comparing OpenAI and Anthropic, it is crucial to look beyond headline valuation figures and consider fundraising timing, revenue metrics, and capital structure.

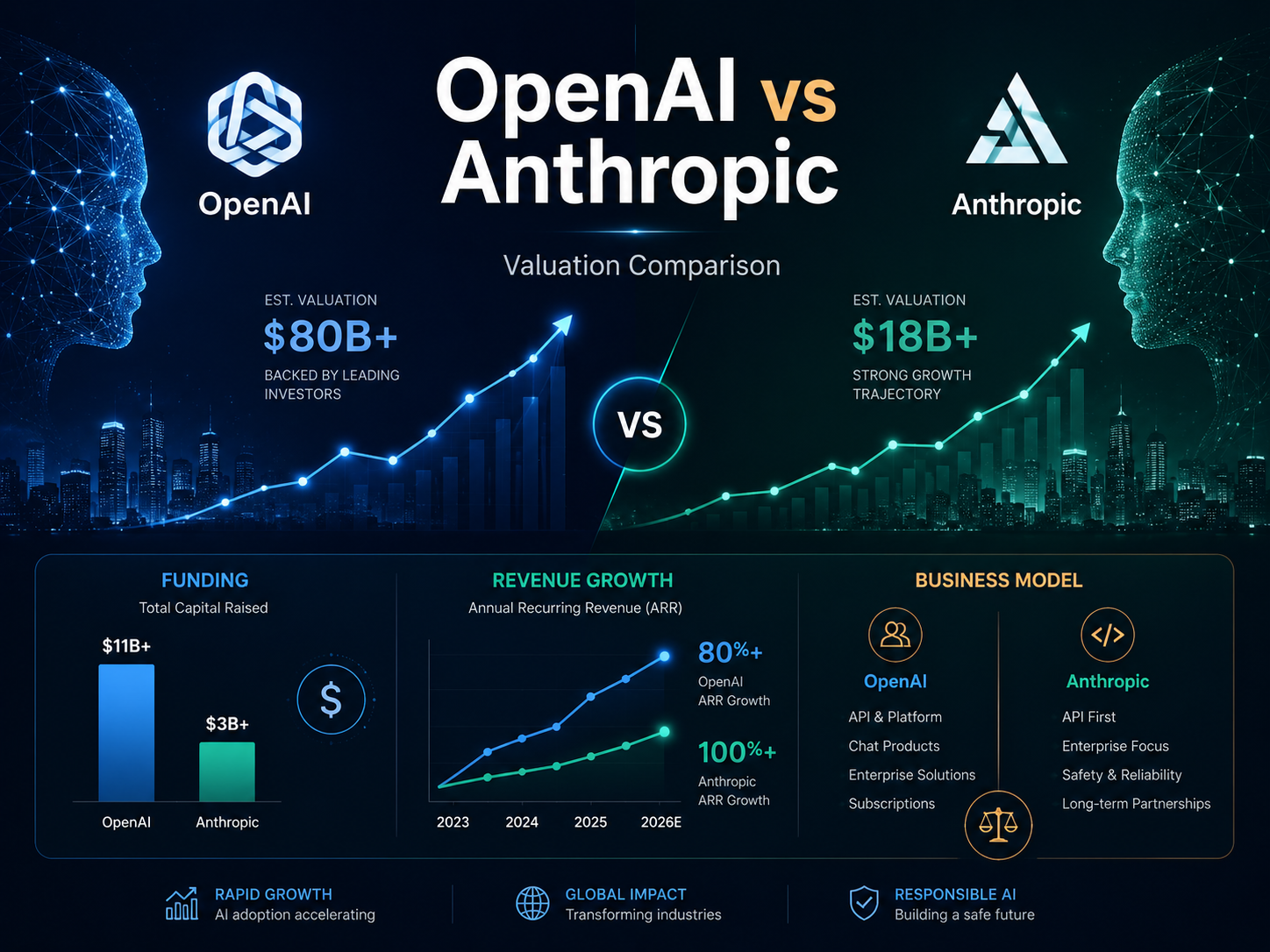

What Are OpenAI and Anthropic’s Current Valuations?

OpenAI closed a $122 billion funding round in March 2026, reaching a post-money valuation of $852 billion. The company stated the capital would be used to expand hashrate capacity, drive model R&D, and support further growth in ChatGPT, enterprise products, API, and developer tools.

Anthropic raised $65 billion in its Series H round in May 2026, achieving a post-money valuation of $965 billion. This round put Anthropic ahead of OpenAI in the latest private pricing. The funds are primarily allocated to expanding compute resources, advancing safety and interpretability research, and scaling the Claude product and partner ecosystem.

| Comparison Metric |

OpenAI |

Anthropic |

| Latest Funding Date |

March 2026 |

May 2026 |

| Latest Funding Amount |

$122 billion |

$65 billion |

| Latest Post-Money Valuation |

$852 billion |

$965 billion |

| Core Products |

ChatGPT, API, Codex |

Claude, Claude Code, Cowork |

| Main Valuation Drivers |

Consumer distribution, enterprise deployment, developer platform |

Enterprise adoption, programming tools, agent workflows |

Because Anthropic’s fundraising occurred after OpenAI’s, its valuation reflects more recent revenue and market expectations. If OpenAI were to raise funds at the same time, the pricing dynamic could shift. Therefore, “Anthropic’s higher valuation” only reflects the latest public fundraising context.

How Have OpenAI and Anthropic’s Valuations Evolved?

OpenAI’s valuation has been largely driven by the global adoption of ChatGPT. In its 2026 fundraising announcement, OpenAI revealed that ChatGPT was nearing 1 billion weekly active users and had expanded from a consumer assistant into enterprise workflows, APIs, and software development. This broad distribution capability has been a major foundation for OpenAI’s high valuation.

Anthropic’s valuation growth was more concentrated in 2026. The company’s valuation rose from $380 billion in February to $965 billion in May—more than doubling in just three months. During this period, Anthropic reported its annualized revenue run rate jumped from $14 billion to over $47 billion, with rapid expansion of enterprise customers and Claude Code driving the valuation surge.

These two valuation curves reflect distinct growth paths. OpenAI first built broad user coverage with ChatGPT, then accelerated its expansion into enterprise and developer markets. Anthropic, by contrast, quickly scaled revenue through enterprise APIs, programming tools, and agent workflows, achieving a new valuation premium with higher recent growth.

How Does Revenue Scale Support OpenAI and Anthropic’s Valuations?

In March 2026, OpenAI disclosed monthly revenue of $2 billion, translating to a simple annualized figure of about $24 billion. The company also noted that by the end of 2024, quarterly revenue was around $1 billion, indicating that ChatGPT subscriptions, enterprise products, and API usage continued rapid growth.

In May 2026, Anthropic revealed its annualized revenue run rate had surpassed $47 billion, up from $14 billion during its February fundraising. This figure reflects annualized revenue at a point in time, not audited full-year revenue, but it does demonstrate rapid short-term growth in Claude’s enterprise and developer adoption.

Revenue run rates should not be compared directly without considering the underlying metrics. OpenAI reports current monthly revenue and its trajectory, while Anthropic reports an annualized run rate; both may use different methodologies for channel splits, cloud sales, and API revenue recognition. Thus, Anthropic’s current growth rate appears faster, while OpenAI has built a broader user and product base.

How Do Consumer and Enterprise Businesses Drive Different Valuation Models?

OpenAI’s valuation is anchored in ChatGPT’s massive consumer reach. Its vast individual user base can be converted into paid subscriptions, brand recognition, and enterprise adoption, while also providing a low-cost funnel for APIs, Codex, and other work tools. OpenAI describes this as a growth flywheel connecting consumer reach, enterprise deployment, developer usage, and hashrate.

Anthropic’s revenue structure is more focused on enterprise and developer markets. As of February 2026, the company reported more than 500 customers with annualized spending above $1 million, and 8 of the Fortune 10 companies using Claude. The number of customers with annual spending above $100,000 grew sevenfold in one year.

Consumer businesses typically offer larger potential markets and distribution advantages but face challenges like free user costs, paid conversion, and retention. Enterprise contracts are larger and have higher switching costs but may lead to customer concentration, longer sales cycles, and reliance on a few high-value workflows.

How Do ChatGPT and Claude’s Product Positioning Influence Market Expectations?

ChatGPT targets consumers, enterprise employees, and developers. OpenAI generates multiple revenue streams through personal subscriptions, business and enterprise seats, API usage, and tools like Codex. By the end of 2025, OpenAI reported over 1 million enterprise customers and more than 7 million workplace seats.

Claude’s growth is centered on programming, enterprise knowledge work, and agent-driven tasks. Claude Code can read code repositories, modify files, execute commands, and integrate with development tools; Anthropic has also extended it to finance, sales, cybersecurity, and knowledge work scenarios.

Claude Code’s annualized revenue exceeded $2.5 billion in February 2026, more than doubling since the start of the year, with enterprise customers accounting for over half of that revenue. This high-value, high-frequency developer tool business is a key factor in Anthropic’s rapid valuation gains over OpenAI.

How Do Microsoft, Amazon, and Google Impact Both Companies’ Valuations?

OpenAI’s partnership with Microsoft provides cloud infrastructure, enterprise sales channels, and capital support. OpenAI’s current valuation also depends on its ability to expand independent hashrate, developer platforms, and enterprise products. Investors are watching whether the company can reduce dependency on a single infrastructure provider while maintaining key partnerships.

Anthropic has close ties with Amazon and Google, enabling Claude to reach enterprise customers via partner cloud platforms. Its latest fundraising included $15 billion in commitments from hyperscale cloud providers, with Amazon pledging $5 billion. Infrastructure partners like Micron, Samsung, and SK hynix also participated.

Cloud partnerships offer chips, data centers, sales channels, and enterprise customers, but also create revenue sharing, hashrate procurement, and strategic dependencies. Investors are concerned not just with cloud support, but also with how much gross margin and customer control model companies can retain.

How Do Hashrate Costs and Capital Needs Affect Valuation Sustainability?

Hashrate is a fundamental constraint for both OpenAI and Anthropic’s high valuations. Training advanced models, serving massive user bases, and running autonomous agents all require continuous investment in chips, power, data centers, and networking—so revenue growth does not guarantee improved profitability.

OpenAI’s $122 billion and Anthropic’s $65 billion fundraising rounds far exceed those of traditional software companies. Both have prioritized expanding compute capacity, highlighting that competition is now about capital and infrastructure, not just models and products.

High valuations enable companies to raise more capital with less equity dilution but also raise the performance bar for future fundraising or IPOs. If revenue growth slows, inference prices fall, or open-source models close the gap, investors may reassess whether such large-scale hashrate investments can deliver sustainable returns.

How Should OpenAI and Anthropic’s Valuations Be Compared?

Valuations cannot be judged simply by “valuation divided by revenue.” Private companies do not report revenue under unified accounting standards, and fundraising terms may include liquidation preferences, anti-dilution, and other rights—so headline multiples are not strictly comparable.

| Comparison Dimension |

OpenAI |

Anthropic |

| Latest Public Valuation |

$852 billion |

$965 billion |

| Core Distribution Advantage |

Global consumer reach via ChatGPT |

Deep enterprise and developer adoption |

| Main Revenue Model |

Personal subscriptions, enterprise seats, API, developer tools |

Enterprise API, Claude subscriptions, Claude Code, agent tools |

| Recent Revenue Signals |

Monthly revenue ~$2 billion |

Annualized run rate >$47 billion |

| Main Growth Drivers |

User scale, enterprise conversion, API & Codex |

Claude Code, enterprise clients, agent workflows |

| Main Infrastructure Partners |

Microsoft and diverse hashrate partners |

Amazon, Google, and chip partners |

| Valuation Strengths |

Broad reach, strong brand, diverse products |

Rapid growth, high enterprise revenue concentration |

| Main Valuation Pressures |

Strategic focus, hashrate costs, commercialization efficiency |

Growth sustainability, client mix, expansion costs |

Current data shows Anthropic has achieved a higher private valuation and faster revenue growth signals, while OpenAI retains greater consumer reach, a broader product suite, and a larger enterprise customer base. These companies represent two distinct AI platform business models—not identical assets.

What Challenges Do OpenAI and Anthropic Face at High Valuations?

OpenAI’s main challenge is maintaining strategic focus across consumer, enterprise, programming, agent, and multimodal products. Reuters cited investor concerns about OpenAI’s frequent product roadmap changes under competitive pressure; the market is watching whether its enterprise business and Codex can further support its $852 billion valuation.

Anthropic must prove its recent hyper-growth is sustainable. Its annualized run rate surged in a short time, possibly due to a few large clients, compute supply, and Claude Code’s momentum. If client expansion slows, a near-trillion-dollar valuation will demand even higher revenue quality and profitability.

Both companies face converging model capabilities, falling API prices, open-source competition, regulatory shifts, and high hashrate costs. High valuations reflect investor expectations for the long-term future of AI infrastructure and work platforms, but do not guarantee short-term profits, IPO pricing, or future returns.

Summary

As of May 2026, Anthropic’s latest post-money valuation of $965 billion surpasses OpenAI’s $852 billion. Anthropic’s edge comes from rapid growth in Claude Code, enterprise clients, and annualized revenue run rate. OpenAI’s core value is rooted in ChatGPT’s global reach, enterprise customer base, API platform, and multi-product ecosystem.

The valuation gap between OpenAI and Anthropic fundamentally reflects the market’s differing views on two business models. OpenAI is evolving from a consumer platform toward enterprise infrastructure, while Anthropic is expanding from enterprise models and developer tools toward a universal work platform.

Comparing the two requires a holistic view of revenue metrics, client structure, product stickiness, hashrate costs, and funding terms. Latest private valuations reflect current market sentiment but do not substitute for assessments of profitability or long-term competitive advantage.

FAQ

Are OpenAI and Anthropic’s Valuations the Same as Public Market Caps?

No. OpenAI and Anthropic’s valuations are post-money figures based on their latest private fundraising rounds and are not traded in real time like public company stocks.

Why Do Later Fundraising Rounds Often Command Higher Valuations?

Later-stage companies can use more recent revenue and growth data for pricing and are influenced by prevailing capital market sentiment. As a result, valuations from different fundraising rounds are not directly comparable.

Is Annualized Revenue Run Rate the Same as Actual Full-Year Revenue?

No. The annualized run rate is a projection based on current monthly or quarterly revenue. If growth or usage changes, actual full-year revenue may differ from the run rate.

Does Anthropic’s Higher Valuation Mean Claude Has More Users?

No. Anthropic’s higher valuation does not mean Claude has more users overall. ChatGPT still commands broader consumer reach, while Anthropic’s valuation currently emphasizes enterprise revenue growth and developer tool performance.

How Will High Valuations Affect Future IPOs?

High valuations raise the benchmark for future IPO pricing and increase pressure to deliver revenue, profit, and sustained growth. If public markets assign a lower valuation, the company may face a down round.

Can Regular Investors Buy OpenAI or Anthropic Stock Now?

No. Regular investors generally cannot buy OpenAI or Anthropic shares on public markets at this time, as both remain private companies with equity circulating mainly through private placements.