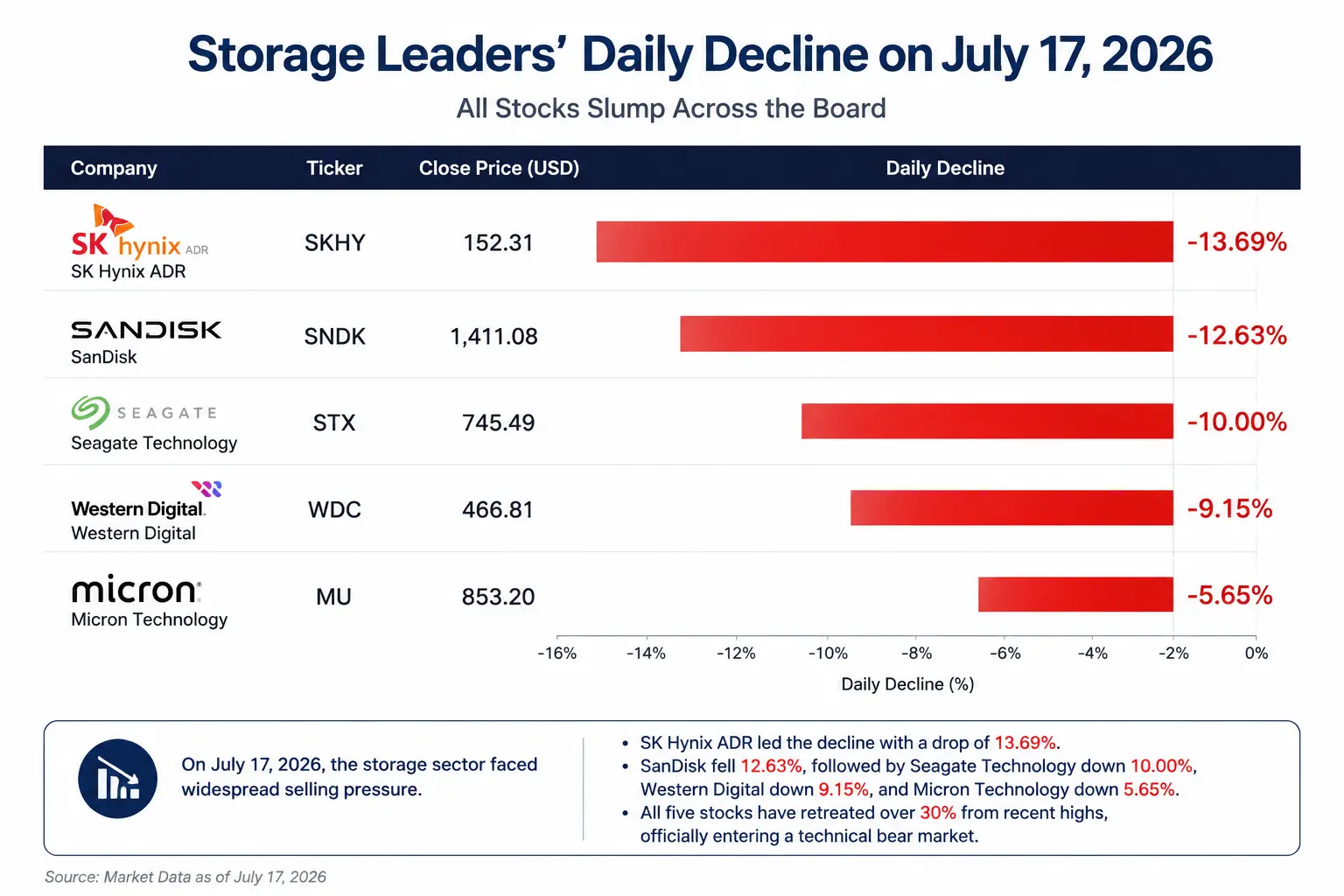

All four storage bellwethers have fallen more than 30% from their recent highs, and all of them have slipped into a technical bear market. Meanwhile, the three major US stock indexes closed lower across the board: the Dow fell 0.2% to 52,552.97, the Nasdaq fell 1.47% to 25,881.95, and the S&P 500 fell 0.51% to 7,533.76. However, Apple surged 4.01%, Alphabet rose 3.60%, Meta gained 3.07%, Amazon rose 3.02%, and Microsoft climbed 2.78%—the five biggest tech giants were all green. The market showed a rare divergence: “software tech holding up the tape, while hardware semiconductors plunged.”

This is not a simple case of sector rotation. Behind Seagate’s 10% single-day drop lies a deep reshaping of the market’s logic for AI infrastructure investment: capital is shifting away from the narrative of “AI infrastructure growing infinitely,” and toward reassessing the sustainability of AI capex and how value is distributed across each link of the industrial chain.

July 17 single-day跌幅 comparison for storage bellwethers

South Korea tightens leverage ETF regulation: the fuse that ignited the sell-off

This round of selling first started in Asia. On July 16, South Korea’s Financial Services Commission (FSC) officially announced tighter regulatory measures for single-stock leveraged ETFs: raising the minimum margin threshold for retail investors from 10 million won to 30 million won, allowing margin to be used only in cash, limiting single-stock leveraged trades to a maximum purchase of 20 shares per transaction, and pausing the launch of new single-stock leveraged products.

This regulatory move precisely targeted the most active source of leveraged funds in storage-stock trading. Over the past year, driven by demand for AI servers and HBM, storage bellwethers such as Micron and SK hynix became key bets for South Korean retail investors and leveraged-ETF capital. Because leveraged ETF products must adjust holdings daily to maintain a fixed leverage ratio, when the underlying stock falls, they are often forced to sell further—creating a negative feedback loop of “stock prices decline → product reduces positions → sell-off intensifies.”

JPMorgan analyst Nikolaos Panigirtzoglou said: “Since reaching a peak in June, AUM of storage-chip leveraged ETFs has shrunk by 34%, while all leveraged stock ETFs combined have only fallen 13% over the same period.” The leveraged ETF assets as a proportion of the related companies’ market cap are about three times that of plain equity ETFs, making them an important amplifier of industry volatility.

However, South Korea’s regulation was only the direct trigger for the selling pressure. A deeper market concern is that the stocks of the “four storage giants” had already priced in—far ahead of time—optimistic scenarios around HBM shortages, product price hikes, and the long-term rapid growth of AI server demand. Once investors start worrying about capex for expansion pace, improvements in equipment efficiency, or a slowdown in cloud vendors’ capital expenditures, any fundamental noise could trigger a sharp valuation reset.

Seagate’s role in the industry chain: AI data infrastructure, not the core of AI computing

To understand why Seagate is taking such a large hit in this sell-off, you first need to clarify its true position in the AI industry chain.

Seagate Technology’s core business is mechanical hard disk drives (HDDs). Its AI beneficiary logic does not come from computing chips required for AI model training, but from data center expansion demand driven by the explosive growth of AI data. AI model training generates massive volumes of data—from training datasets and model checkpoints to inference logs and user interaction records—which ultimately must be stored persistently.

Seagate’s fiscal year 2026 third-quarter results show revenue of $3.11 billion, with the data center business contributing $2.5 billion in revenue, up 55% year over year, accounting for 80% of total revenue. Hard drive shipments reached 199 exabytes (EB), up 39% year over year, with about 90% going to data center customers. Nearline HDDs account for nearly 90% of total shipments and have become a core driver of large-scale AI storage.

From an industry-chain transmission perspective: AI model training demand increases → GPU server purchases rise → HBM high-speed memory demand increases → data center expansion → enterprise storage demand is released → HDD procurement increases. Seagate sits at the very end of this chain.

This is the key issue. When the market starts reprioritizing AI capex, investors naturally ask: if AI budgets face pressure, will funds be prioritized for GPUs and HBM—or for HDDs?

AI data center demand: a clash between long-term logic and near-term worries

Bull case: structural support from storage shortages

The core logic supporting Seagate’s long-term growth has not been broken by a single-day rout.

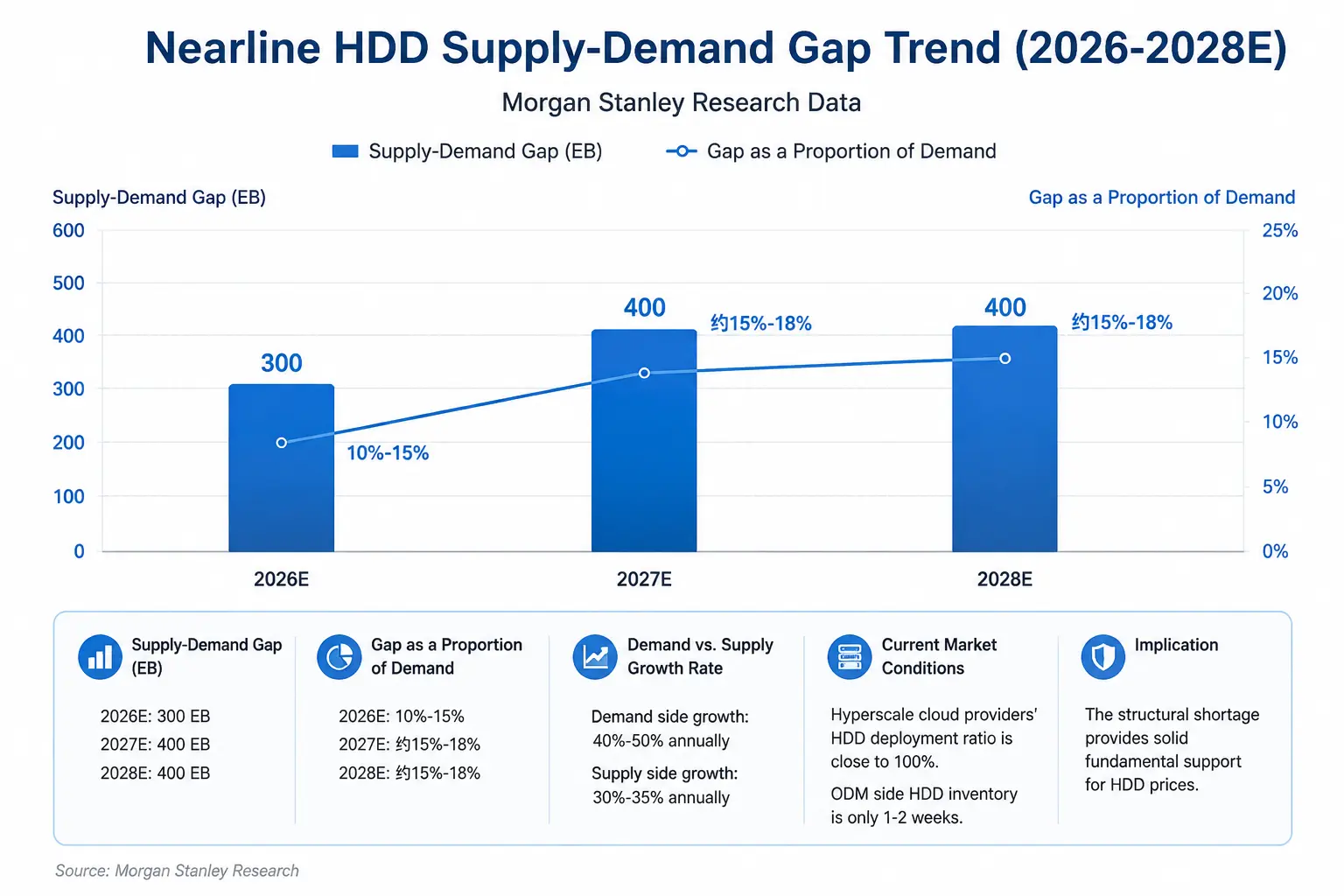

From supply-and-demand fundamentals, the storage industry is in a rare structural shortage cycle. Morgan Stanley’s research shows HDD demand is currently growing at 40% to 50% per year, while supply growth is only 30% to 35%. In 2026, the supply of nearline HDDs will be short by about 300EB (exabytes) relative to demand—roughly a 10% to 15% gap. The gaps in 2027 and 2028 further widen to around 400EB each year. Analysts noted: “The hard drive cycle is getting longer—shortages are expected to last at least through 2028—while this also indicates that hard drive prices are strengthening in a clear and meaningful way.”

On the demand side, cloud service providers’ capital expenditures are still expanding. Morgan Stanley expects that AI data center spending by five mega cloud providers—Meta, Amazon, Alphabet, Microsoft, and SpaceX—will reach about $1.2 trillion in 2027, rising further to $1.4 trillion in 2028. On July 10, Wells Fargo raised Seagate Technology’s rating from “Hold” to “Buy,” lifting its target price from $900 to $1,100. On July 14, Citigroup raised its target price to $1,240 and maintained a “Buy” rating. On July 16, JPMorgan raised its target price from $920 to $1,095. On July 1, Bank of America raised its target price from $1,000 to $1,150.

From a capacity perspective, Seagate management has confirmed that nearline capacity is locked in through 2027. Some analysts even believe HDD shortages may continue through 2028.

Nearline HDD supply-demand gap trend (2026-2028E)

Bear case: doubts about the sustainability of AI capex

However, the market is actively debating another set of questions.

First, is the growth slope of AI capex approaching an inflection point? JPMorgan predicts that the five cloud service providers (Google, Amazon, Meta, Microsoft, and Oracle) will reach $75.81 billion in capital expenditures in 2026, doubling year over year, and rising to $92.50 billion in 2027—but the growth rate is expected to sharply slow down to 22% starting in 2027. The market is starting to worry: if AI commercialization and monetization don’t happen as quickly as expected, will cloud vendors cut capex after 2027?

Second, cyclical risks inherent to the storage industry. The storage industry has long had a cycle of “supply-demand cycle → price increases → capacity expansion → inventory build-up → price declines.” Even though HDD is currently in a shortage state, once AI demand growth slows or capacity expansion accelerates, enterprise inventories could increase, the upside room for storage price increases could shrink, and earnings expectations would be lowered.

Third, valuation-related pressure. After a surge through 2026 so far—Seagate’s stock price has at one point jumped by about 269% year to date—any uncertainty in fundamentals could trigger a dramatic valuation reset in a very short period of time. All four storage bellwethers are down more than 30% from their recent highs, which in itself suggests that extremely high market expectations were already embedded in the earlier rally.

Value layering across the AI storage chain: who’s at the core, who’s on the periphery?

Across different segments of the AI storage industry chain, companies face materially different AI beneficiary logic and current risks.

SK hynix’s core business is HBM (high-bandwidth memory). This is an indispensable companion chip for AI GPUs—especially NVIDIA products—and is directly involved in the core part of AI computing. Its AI beneficiary logic is the most direct—HBM is a must-have for stacking AI training compute. The risks are also pronounced: the valuation correction pressure is huge, and it must continuously fend off expansion threats from competitors such as Samsung.

Micron Technology covers both DRAM and HBM. It benefits from rising AI server memory demand, but it is also constrained by cyclic volatility in the traditional memory market. Its position in the chain sits between core and peripheral.

Seagate Technology’s core business is HDD mechanical hard drives, placing it in the infrastructure layer of AI data storage. Its AI beneficiary logic comes from storage demand driven by data center expansion, but it is a “downstream catch” stage of AI investment, ranked after GPUs, HBM, and AI servers. The key core risk right now is that if AI capex growth slows at the margin, HDD could be one of the first procurement items to be compressed.

Western Digital covers both HDD and NAND flash. Its business structure sits between Seagate and pure-play flash manufacturers, and it also faces dual pressure from both the HDD supply-demand logic and the NAND price cycle.

Key variables for Seagate’s future trajectory

First, the actual execution pace of cloud vendors’ capital expenditures. The biggest disagreement in the market is not whether cloud vendors will increase capital expenditures in 2026, but whether the growth rate after 2027 will slow more than expected. Seagate’s results are highly dependent on data center demand, and any downward revision to cloud vendors’ capex guidance could hit the stock directly.

Second, the share of AI-related revenue and changes in gross margin in the next quarter’s earnings report. Seagate’s fiscal year 2026 third-quarter gross margin has reached 47%. The market will focus intensely on whether this gross margin level can be maintained, and whether management’s forecast for 2027 demand is adjusted.

Third, the actual evolution of HDD pricing and the supply-demand gap. Morgan Stanley expects an HDD supply gap of about 300EB in 2026, but that forecast is built on assumptions of 40% to 50% annual demand growth and 30% to 35% annual supply growth. Any on either side that deviates beyond expectations would change the HDD pricing environment.

Fourth, a reshaping of the overall valuation framework for the storage industry. All four storage bellwethers have fallen more than 30% from recent highs and have all entered a technical bear market. Whether this sell-off implies that storage stocks are switching from an “AI narrative-driven” framework back to a “cyclical stock valuation framework” will determine the valuation anchor logic for Seagate over the next several quarters.

Seagate’s single-day 10% plunge is not just a one-off market sell-off—it is a valuation reassessment after AI infrastructure investment enters a second phase. In this phase, investors are re-evaluating how value is allocated among GPUs, HBM, and storage equipment: who is positioned at the core priority of AI investment, and who may be pushed to the margins when the accounting doesn’t add up economically. For Seagate, the continued widening of the HDD supply-demand gap provides solid fundamental support. But a potential slowdown in AI capex growth and the inherent cyclical characteristics of the storage industry are becoming two swords hanging over valuation. The fact that all storage bellwether stocks have fallen into a technical bear market shows that the market is demanding these companies prove—through consistently performance that beats expectations—that AI storage demand is not just a short-lived replenishment cycle, but a true structural turning point.

FAQ

Q1: What is the direct reason for Seagate Technology’s 10% stock price plunge on July 17?

South Korean regulators tightened oversight of single-stock leveraged ETFs, raising the minimum margin requirement from 10 million won to 30 million won, triggering passive position reductions in leveraged storage-stock products. Combined with market worries about the sustainability of AI capex and the large gains already accumulated in storage stocks earlier, selling pressure quickly transmitted from the Korean market to US stocks, and Seagate Technology closed down 10% to $745.49.

Q2: What’s the difference between Seagate Technology and AI chip companies?

Seagate is not an AI chip company; it is an AI data storage infrastructure company. Its beneficiary logic comes from enterprise HDD demand driven by data center expansion, placing it in the storage layer of the AI industry chain, behind GPUs, HBM, and AI servers in priority. When the market re-evaluates AI investment priorities, HDD is often viewed as the segment most likely to be compressed.

Q3: Is demand for HDD from AI data centers really declining?

Current data does not support the view of declining demand. Morgan Stanley expects a nearline HDD supply gap of about 300EB in 2026, and the gap expands to 400EB in 2027 and 2028. Demand grows 40% to 50% per year, far exceeding supply growth. Cloud vendors’ capex is still expanding; Morgan Stanley expects AI spending by the five largest cloud providers to reach $1.2 trillion in 2027.

Q4: What are the latest ratings and target prices from analysts for Seagate Technology?

Multiple investment banks raised Seagate’s target price before the sell-off: Citigroup raised it to $1,240 (Buy), JPMorgan raised it to $1,095 (Overweight), Wells Fargo raised it to $1,100 (Buy), and Bank of America raised it to $1,150 (Buy). S&P Global’s survey of 25 analysts shows a consensus rating of “Strong Buy,” with an average target price of $992.74.

Q5: What stage is the supply-demand cycle in the storage industry currently in?

It is in a structural shortage stage. HDD demand is growing 40% to 50% per year, while supply is growing only 30% to 35%, and the supply-demand gap keeps widening. Industry institutions expect this round of price increases to extend into 2027. Morgan Stanley’s research indicates HDD shortages are expected to last at least through 2028.