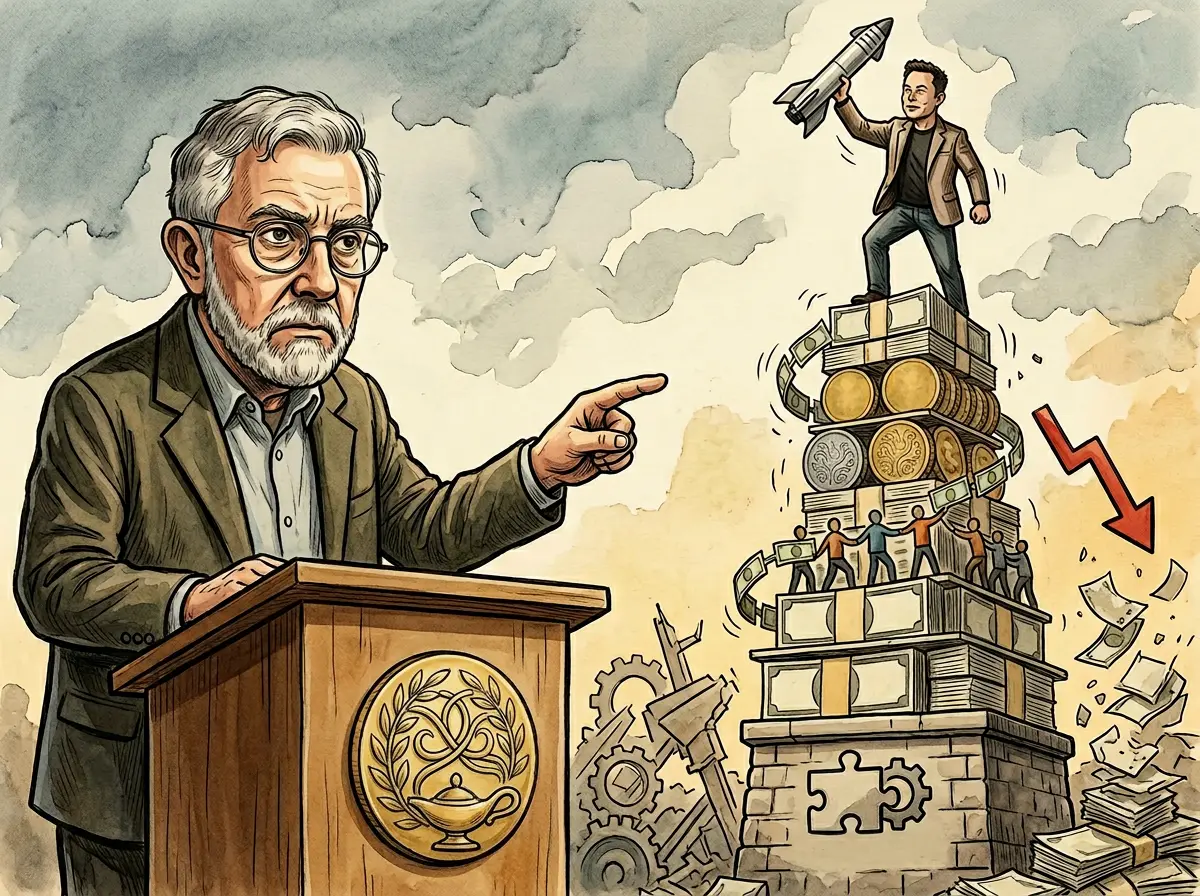

Nobel Prize-winning economist Paul Krugman published an article on June 15 on his personal Substack column, describing Musk as a “Ponzi scheme for humanity,” focusing on SpaceX, which recently went public. In SpaceX’s lofty valuation, a large premium comes from Musk’s personal charisma and imagination about the future—far beyond what the rocket launch and satellite communications businesses themselves can reasonably support.

Krugman’s Core Argument: Brand Premium and Untethered Vision

The following are Krugman’s personal commentary positions and do not represent market consensus, official regulatory conclusions, or legal opinions:

Musk’s Premium and Capital Narrative: Krugman believes that over the years, Musk has built a capital narrative around his personal brand and future vision. The market’s willingness to keep putting money in largely stems from trust and expectations of him personally, rather than valuation based purely on existing operating results.

Unrealized Vision Checklist: Krugman lists plans that have not fully materialized to date: Hyperloop (high-speed pipeline transportation), widespread adoption of fully autonomous driving, commercialization of brain-machine interfaces, and colonization of Mars. He notes that these plans have not clearly weakened investors’ confidence in Musk.

Spillover Effects of SpaceX’s IPO: Krugman argues that by listing SpaceX, Wall Street brought the high valuations and Musk premium that previously existed only in private markets into the public market, allowing more retail investors to participate.

Risk of Valuation Reassessment: Krugman warns that once the market begins to re-evaluate the realizability of these visions, valuations built on high confidence could face dramatic corrections.

SpaceX Achievements Acknowledged by Krugman

In the critical article, Krugman himself explicitly acknowledges the following confirmed SpaceX achievements: SpaceX has become an important participant in the global commercial aerospace industry; and the Starlink satellite network has established an actual commercial model and revenue source.

Krugman’s argument is not denying the above achievements. Instead, he claims that the valuation scale currently granted by the market exceeds what these commercial achievements alone can support, including a large amount of premium that cannot be measured by existing fundamentals.

Reactions from All Sides: Supporters vs. Critics

According to reports, Krugman’s article prompted two types of responses (sources unnamed):

Those Supporting Krugman’s Position: Some people believe Krugman pointed out a problem in technology markets in recent years—overreliance on narratives and celebrity effects. High valuations often rest on believing in future growth stories, rather than the company’s actual ability to profit at present.

Those Criticizing Krugman’s Position: Supporters of Musk say SpaceX has successfully reduced rocket launch costs, helped popularize reusable rocket technology, and built one of the world’s largest low-Earth-orbit satellite networks. These are real commercial achievements and cannot be explained solely by market hype.

Word Choice Limits (Krugman’s Clarification): In the article, Krugman clearly stated that the use of the term “Ponzi scheme” is more of a commentary-based metaphor, mainly expressing that some valuations depend on continuously attracting new capital, rather than accusing anyone of illegal conduct.

Common Questions

Did Krugman’s claim that SpaceX is a “Ponzi scheme” constitute an accusation in a legal sense?

No. According to reports, Krugman himself clarified in the article that “a Ponzi scheme for humanity” is a rhetorical metaphor for commentary, not an accusation that SpaceX or Musk is involved in any illegal financial fraud. This is a critical commentary on valuation models, not a legal accusation of unlawful conduct.

Does Krugman’s criticism deny SpaceX’s technological achievements?

No. In the article, Krugman explicitly acknowledged that SpaceX has become an important participant in global commercial aerospace, and Starlink has established an actual commercial model and revenue. The core of his criticism is whether the valuation scale matches existing fundamentals, not whether the technology capabilities are real.

What is the core disagreement behind the market’s polarized reactions to Krugman’s criticism?

According to reports, the side supporting Krugman focuses on whether current profit-generating ability can support high valuations. The side criticizing Krugman emphasizes that SpaceX has real, on-the-ground commercial achievements (reusable rockets, Starlink commercialization). This reflects a long-standing logic split in capital markets: pricing based on existing fundamentals, or pricing based on future market potential.